Let's Use Financial Engineering for Good, with a New Structured Product

At a time of difficulty, due to COVID-19 and climate change, innovative financial products are needed: for example, one that offers great liquidity and flexibility so that banks in Latin America and the Caribbean can reach social impact and climate commitments.

The conventional response to an economic crisis – such as the one caused by the current pandemic – involves increasing liquidity by boosting credit. But this creates risks that cannot be ignored.

These risks include not only the most obvious, such as the possibility of excessive financial sector exposure, but others that are less obvious. Such as, for example, that in the process of stimulating the economy, fundamental principles that go beyond financial matters are forgotten, including the fight against climate change.

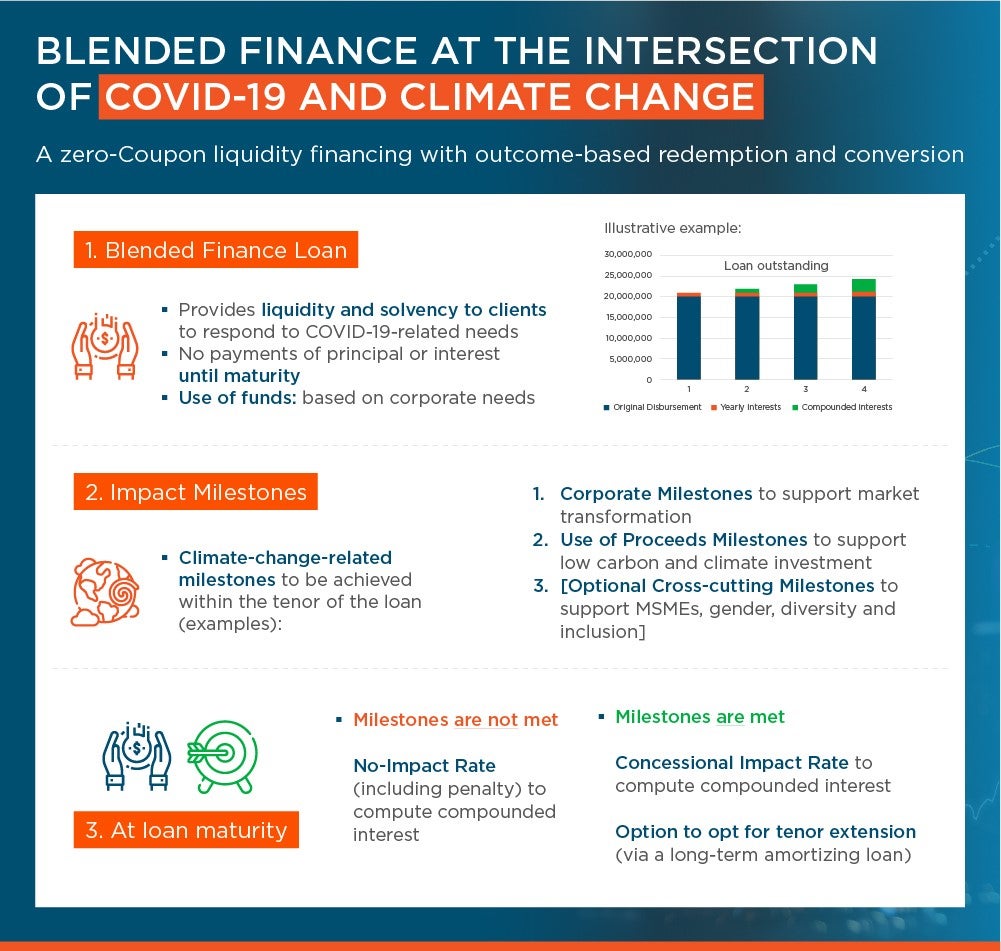

To resolve this tension, a possible solution is the use of blended finance products, including one that we have created for banks in Latin America and the Caribbean. The product is, in financial-speak, a subordinate zero coupon structure that strengthens the borrower's capital position.

For non-experts, the idea is that financial institutions receive funds in the least onerous conditions possible, and at the same time they can make commitments on climate change. Hence the design.

You may also like:

-

Sustainability, the vaccine for Latin America and the Caribbean economies

-

Private Investment, a Solution to Water & Sanitation Challenges in Latin America & the Caribbean

-

Latin America & the Caribbean Has a Truck Problem, But the Solution is on its Way

The product has two fundamental characteristics: the first is that it can be subordinate – that is, it may have a lower collection priority for the holder than those contracted with other creditors. This debt is similar to capital so it is computed, according to each country's regulation, as capital in the borrower's accounts.

The second feature is tied to the zero coupon. This means that the financial institution that has contracted this product does not pay any interest or return any cash during the life of the loan. At maturity, principal and interest are paid on time, but not before.

There's more. And here we enter the part that includes significant innovation related to a series of objectives that the borrower, the financial institution, accepts when signing the contract.

These objectives, which are presented not as covenants or mandatory conditions, but as incentives, refer specifically to the principles we want to enact: for example, that the financial institution joins the Task Force on Climate-Related Financial Disclosures (TCFD) and follows the TCFD recommendations on how to analyze and report exposure to financial risks associated with climate change. Another concrete milestone is that the percentage of the borrower's total loan portfolio that is earmarked for deals that generate positive environmental impacts, such as the reduction of greenhouse gas emissions, is increased.

The borrower has an interest in including these objectives in the contract, because there is no penalty for non-compliance – since they're not mandatory – so it has flexibility; but, if it meets the objectives, this results in a reduction of the interest payable: that is, hard cash savings.

We have created this product, for the first time in IDB Invest's history, with the aim of offering it to the financial sector, including not only banks but also credit institutions, including – possibly – fund management companies. With this product we want to encourage changes at the corporate level in the financial sector institutions to achieve desirable climate results; that is, to encourage policies and processes to work for and finance a low-carbon economy that is resilient to climate change.

We aim for institutional change to increase the scope of our work, with measurable and positive impact results for the climate, seeking portfolio growth that is several times greater than the loan amount. The first related transaction has been closed with Davivienda, one of the leading banks in Colombia. But there's potential for many different approaches.

The expression “financial engineering” is often used as a criticism, to refer to complex and innovative products in the financial world that some use to hide losses or pay less tax. We believe that, with this product, we are using financial engineering, finally, for the benefit of all.

Authors

Matthieu Pegon

Matthieu leads the Blended Finance Team at IDB Invest, which he joined in 2017. He is responsible for managing concessional resources that are invested in transformational projects where risks are too high for commercial finance alone. He is the IDB Group’s focal point for blended finance issues. Before joining the IDB Group, Matthieu worked as Structured Finance Senior Specialist for the Green Climate Fund, the largest multilateral climate finance fund. He also worked at BNP Paribas as Vice President in Structured Debt Capital Markets with a focus on Latin America and the Caribbean. Matthieu earned a master’s degree and a bachelor's degree in finance from Grenoble École de Management (France).

Hilen Meirovich

Hilen Meirovich is the Managing Director of Climate and Environment at IDB Invest. Hilen, has over 20 years of experience in climate finance, sustainable infrastructure, and environmental finance, with roles at IDB, IDB Invest, and active speaker at global climate forums. Under her leadership, IDB Invest expanded its climate advisory services, quadrupling climate-related transactions, and building a $10.3 billion climate finance portfolio. Her leadership included spearheading innovative financing mechanisms, resource mobilization, and aligning organizational practices with the Paris Agreement. An example of those innovations as the development of Latin America’s first blue bond, and positioned IDB Invest as a climate leader across MDBs and other international actors. Hilen holds a PhD in Political Science from Georgetown University, an MA in Public Policy from Georgetown University, and an MA in Political Science from Hebrew University of Jerusalem.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeFinancial Institutions

Related Posts

How Santander Brasil and Eco Invest Mobilize Private Capital at Scale

IDB Invest provides financing to Banco Santander Brasil to support sustainable agriculture, land restoration efforts, and resilient infrastructure.

S&P’s AAA Rating Validates IDB Invest’s Strength and Strategic Direction

The AAA rating expands the institution's access to a broader investor base, supporting its ability to finance and mobilize private impact investment in Latin America and the Caribbean.

Beyond the Cash Gap: How Reverse Factoring Is Unlocking Growth for MSMEs

An IDB Invest study in Mexico estimates that adopting reverse factoring is associated with a 27% increase in companies' sales.