Fintech Solutions as a Vehicle to Expand Financial Inclusion in Latin America and the Caribbean

Fintech solutions and digital banking services offer a unique opportunity to serve previously underbanked individuals and SMEs. Though most commercial banks are adopting these solutions, there is an opportunity to deepen the collaboration with Fintech firms in order to close financial inclusion gaps in the region, while promoting responsible finance practices.

A financial sector that does not prioritize financial inclusion cannot spread the benefits of economic growth to all levels of society. In fact, financial inclusion has been recognized as an enabler of 7 of the 17 Sustainable Development Goals. Promoting access to financial products and services triggers innovation, growth and a broader access to international markets.

In the case of individuals and households, proper access to financial services is crucial to make critical investments, such as higher education and mortgage financing, as well as saving for retirement or starting a business. Access to financial services, including insurance products, is also crucial for coping with unexpected and disruptive events, such as a period of unemployment or health related issues, helping the most vulnerable groups avoid financial losses and mitigate the risk of poverty.

Although with high heterogeneity between Latin American and Caribbean (LAC) countries, the region is consistently behind the most advanced economies and Emerging Asia in a wide range of financial inclusion indicators. According to the Enterprise Surveys, access to finance is a major constraint for doing businesses for the region’s small and medium enterprises, or SMEs.

Also, according the 2017 Global Findex, only 51 percent of the household population in LAC have an account at a formal financial institution, much lower than the average for Emerging Asia (78 percent) and the group of advanced economies (96 percent). Moreover, several countries in Latin America and the Caribbean such as Haiti, Nicaragua, El Salvador, Paraguay and Mexico, show account penetration levels like those in Sub-Saharan Africa, the region that groups the poorest countries in the world.

A digital path to financial inclusion

There are several factors that explain these gaps, such as high levels of informality in the region, stringent documentation requirements to open bank accounts, low penetration of financial products such as leasing and factoring, deficiency or nonexistence of credit information services, lack of adequate public registries for real and movable property, and low financial literacy, among others.

These factors hinder financial inclusion as they generate information asymmetries, promote a risk averse financial industry and pushes households and businesses away from the formal financial system.

In this context, the digital transformation that the economies in the region are undergoing, including financial services, are a welcoming sign. Fintech firms appear as a relevant solution, not only to increase financial inclusion, but also competition, innovation and to deepen financial development.

With smartphone penetration increasing exponentially in Latin America and the Caribbean (and in developing countries in general), a growing communications infrastructure and regulators beginning to embrace the importance of these initiatives, there is an increasing opportunity for SMEs and individuals to access basic financial services through different types of technological applications and innovative solutions.

Fintechs and the disruption in the financial sector

The incorporation of Fintechs in Latin America and the Caribbean is having a disruptive effect in the financial sector, as they have successfully ventured into many of the segments that were the traditionally domain of banks.

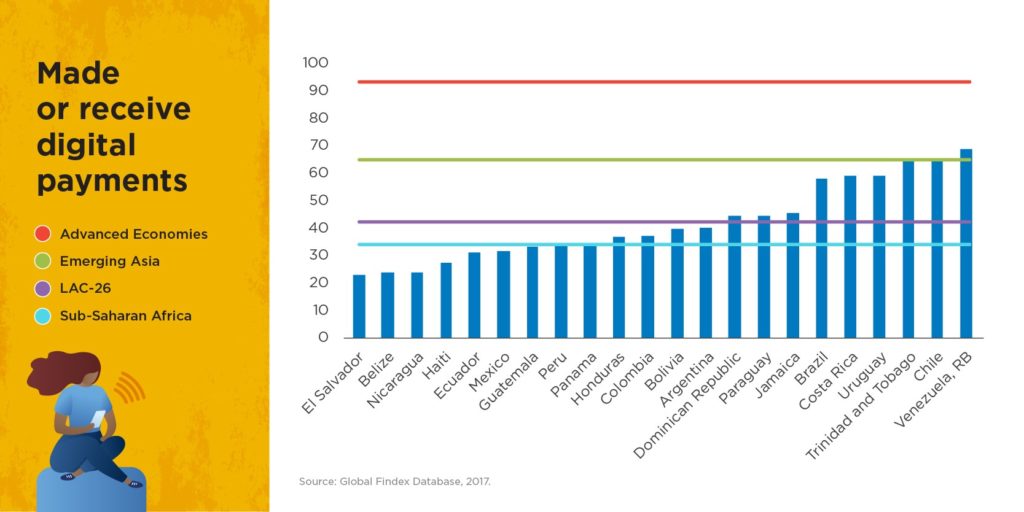

For example, the figure below shows the share of the adult population that made or received digital payments during 2017 in 26 Latin America and the Caribbean countries, compared to regional averages. As previously noted, there is profound heterogeneity of performance between Latin America and the Caribbean countries, and the regional average is much lower than the group of advanced economies as well as Emerging Asia.

[Percentage of population that made/receive digital payments]

It’s worth noting that Venezuela stands out as the country with the highest penetration of digital payments in the region, which is partly explained by the high levels of inflation that have made paper-money transactions almost impossible. Although the Venezuelan case involves a basic financial service (cash transactions), it nonetheless illustrates the power of digital solutions to integrate a wide segment of the population, particularly in a country undergoing a severe economic crisis that has dramatically reduced traditional banking activities.

And even though the Fintech space in the Latin America and the Caribbean region appears to be incipient, it is growing fast. In fact, a recent IDB Study shows that while there were 703 Fintech start-ups in 15 Latin American countries during 2017, that number increased by 66 percent the following year, to 1,166 Fintech start-ups. Payment and remittances, lending, and enterprise financial management are the three largest business segments, followed by personal financial management, crowdfunding and enterprise technologies for financial institutions.

While some commercial banks may perceive the role of Fintech companies as a threat, most of them are embracing these technologies in their product offering, achieving greater efficiencies and increasing the integration of the unbanked population.

Fintechs and digital banking services offer a unique opportunity to serve previously underbanked individuals and SMEs. To seize this opportunity, it is important to have appropriate regulatory frameworks in place that facilitate the incorporation of these technological solutions in an efficient manner.

IDB Invest and the private sector have a role in supporting digital transformation initiatives and deepen the collaboration with Fintech firms to close the gaps of financial inclusion and promote responsible finance practices in the region.

Authors

Joaquin Lennon

Joaquin Lennon has been an economist at the International Monetary Fund's Statistics Department since 2022, where he leads projects to improve data standards and transparency of countries' official economic data. Previously, Joaquín worked as an economist at the Strategy and Development Department of IDB Invest during the years 2018 and 2021, where he contributed to the preparation of the IDB Group’s Country Strategies, among other strategic products, and led the implementation of data-driven tools to identify the of the Group's borrowing countries’ development challenges and to better understand which interventions could generate the greatest development impacts through the private sector. Joaquin is a co-author of numerous knowledge products on Latin American and Caribbean economic development. Other previous positions Joaquín has held include researcher in economic and public policy issues at the University of Chicago, market analyst at Euromonitor International, economist in the Chilean Chamber of Construction's economic studies department, and consultant on policy evaluation projects in Chile, his native country. Joaquin has a master's degree in applied research methods from the University of Chicago, a master's degree in public policy from the University of Chile, and a bachelor's in economics from the same university.

Marcelo Paz

Marcelo Paz is a Bolivian national who joined the IDB Group in 2008. He is currently a lead strategy officer, specialized in development diagnosis of the financial and capital markets sectors. Up until 2015 he was in charge of originating and structuring financial transactions that supported the expansion of financial services in LAC through capital markets development, trade finance and financial intermediaries. Marcelo Paz has over 20 years of experience in the banking and financial markets industry, as well as the public sector. Prior to joining the IDB he worked at commercial banking in Bolivia, where he held different positions, such as Credit Risk Manager and International Business Manager, and was a board member at a brokerage firm and a mutual fund. In addition, he worked at the Bolivian Ministry of Finance, and the Bolivian Stock Exchange. Mr. Marcelo Paz holds an MBA in Finance and Investments from George Washington University.

Terence Gallagher

Terence Gallagher is a British national, based in Washington. He began his career as an investment banker at Citigroup, where he spent 9 years supporting emerging market governments and corporates access the international capital markets, working from London, New York and São Paulo. Since 1999, he has dedicated himself to Microfinance, initially working as a consultant for diverse organizations such as Accion International, Development Alternatives Incorporated, and PlaNet Finance. He joined the IFC in 2008 in Rio de Janeiro where he spent 10 years as a Specialist for Micro and Small Enterprise Finance, responsible for investments in Latin America and Sub-Saharan Africa. As of April 2018, Terence moved to Washington to join IDB Invest as head of Financial Inclusion. He has a Masters degrees in Economics from the University of Cambridge, UK.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeGender

Related Posts

Digital Innovation Expands Financing for Women-Led SMEs in Latin America and the Caribbean

Loans and disbursements approved in less than 24 hours, enabled by artificial intelligence, and early invoice payments powered by fintech solutions are transforming access to credit for MSMEs, especially those led by women.

Fixing the Broken Rung: How Data Can Help Advance Women’s Careers in Latin America and the Caribbean

In Latin America and the Caribbean (LAC), the greatest disruption in women’s career progression occurs during the transition into managerial roles. A collaboration between IDB Invest and LinkedIn, within the framework of the Development Data Partnership, uses large-scale labor-market data to identify where women’s participation declines and what barriers exist across sectors and career stages.

Addressing gender-based violence from the private sector: the experience of Laboratorios Bagó

Francisco Méndez, CEO of the pharmaceutical company, shares his company's efforts and achievements in fostering an inclusive and safe work environment.