Amid the Pandemic, Governments and Multilateral Development Banks Must Continue Supporting Financial Institutions

Governments and multilateral development banks in Latin America & the Caribbean are playing a critical role in supporting financial institutions amid the pandemic, but must be ready to up the ante as the ultimate effects of the lockdown measures become evident in the financial sector, especially key microfinance institutions

As the COVID-19 outbreak wreaks havoc across Latin America and the Caribbean (LAC), many countries are implementing targeted policies to increase liquidity for financial institutions and maintain the flow of credit for businesses and households. That may be critical in stopping the current crisis from spreading to the financial sector.

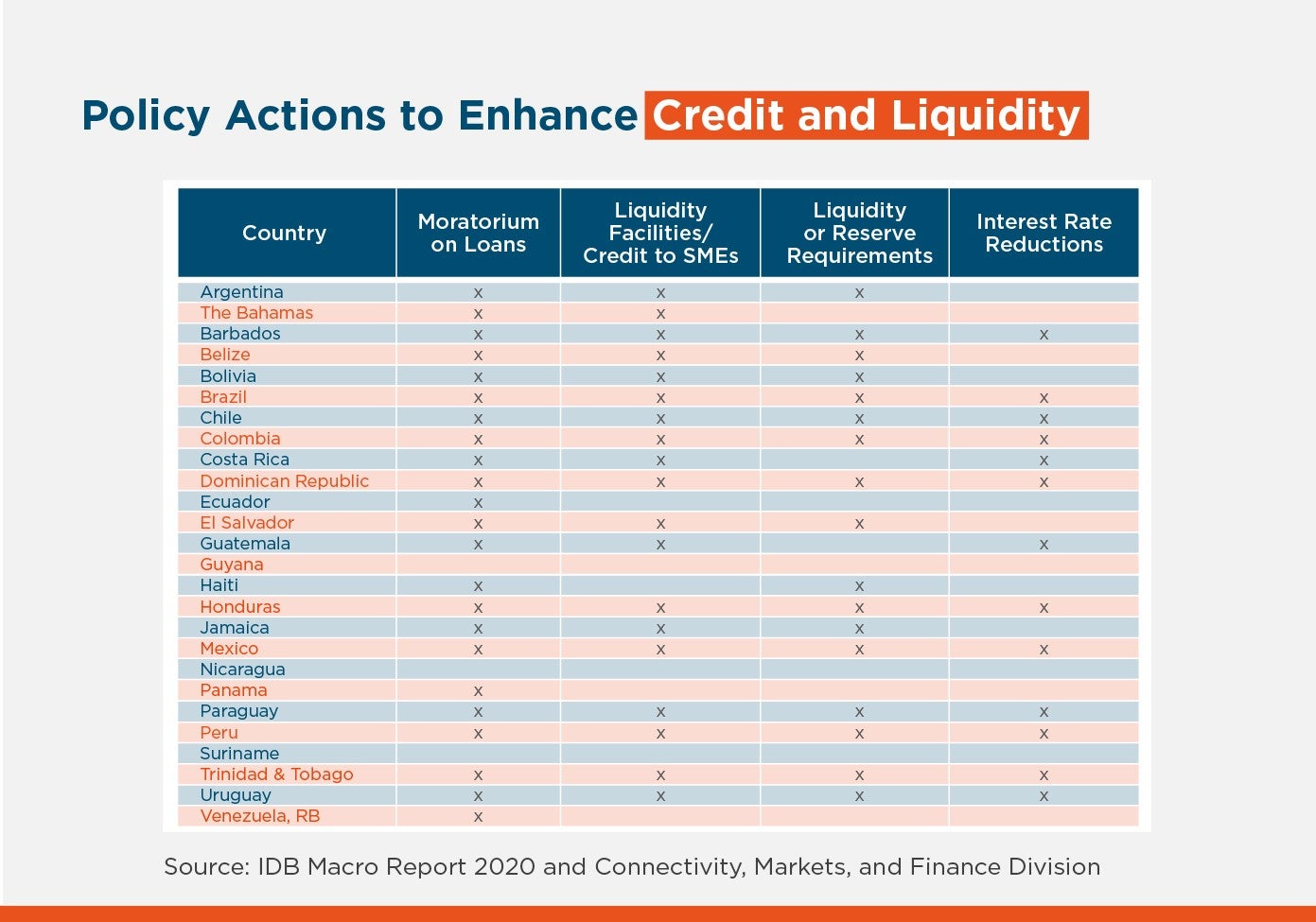

As we discussed in a previous post, LAC financial institutions are, in general, more resilient than they were during the 2008-09 Global Financial crisis, and have a wider reach. Struggling households and businesses affected by strict lockdowns were supported by the right policy mix, which often includes mandated forbearance measures and temporary moratoriums on loans that provided them with some financial breathing space.

Most of these measures were originally in place for three months; however, many were extended through a second round of restructurings that postponed payments for an additional three months and, in some jurisdictions, up to two years. Though these payment extensions come with some regulatory privileges that help financial institutions lower their capital consumption and provision requirements, the quality of the restructured loans could potentially deteriorate in the future, increasing non-performing loans (NPL) and weakening their balance sheets.

The results so far are encouraging, as banks have been able to maintain stability, which limits the potential for systemic risk. However, financial soundness indicators for the second quarter of 2020 illustrate some of the expected impact of the pandemic.

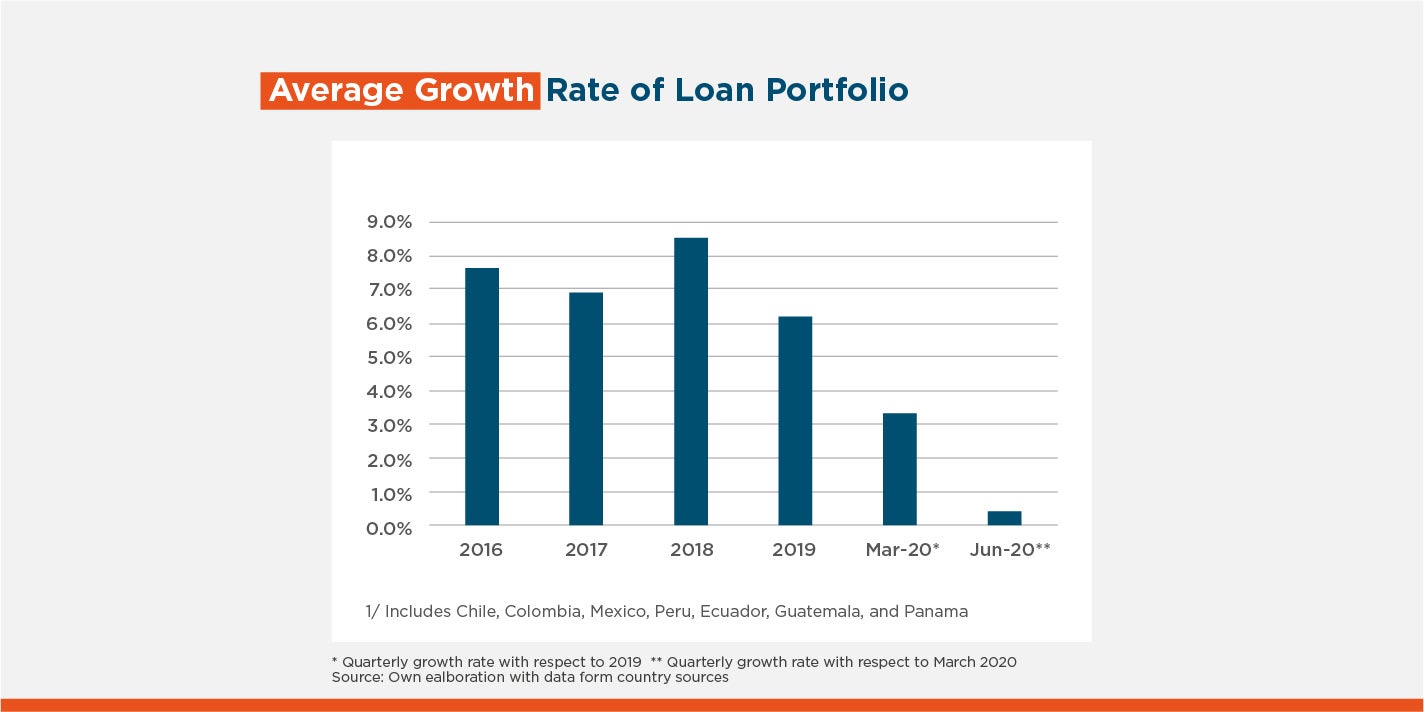

Data for Mexico, Chile, Colombia, Peru, Panama, Ecuador, and Guatemala show a 17% increase in loan-loss provisions in June 2020 with respect to the 2015-2019 average, as banks prepare their balance sheets in anticipation for loan portfolio deterioration. As loan-provision expenses surged, profitability fell almost 30%, with average return on assets and return on equity standing at 1.1% and 10.1% respectively.

Forbearance, loan restructuring, and flexible accounting procedures are keeping NPL and capital adequacy stable for now, at 2.4% and 14.7% respectively. And, as was expected given the widespread lockdown measures, lending activity has been suppressed. The average portfolio growth in the second quarter of 2020 was just 0.4%.

This situation, however, is having a greater impact on microfinance institutions (MFIs), which are in general more vulnerable than commercial banks. A survey carried out by the Consultative Group to Assist the Poor (CGAP, a global partnership of more than 30 leading development organizations) shows that, as of April 2020, two-thirds of MFIs surveyed decreased lending by more than half to preserve liquidity, negatively impacting the low-income communities they serve while hindering financial inclusion efforts.

Moreover, MFIs are exposed to refinancing risk due to their significant reliance on institutional funding, and investors have become more risk averse. CGAP expects that 25% of MFIs globally could face liquidity problems if they are unable to secure refinancing as their funding operations come due; though data for MFIs in the LAC region is not as severe. The average term granted by MFIs on rescheduled loans was three months at the beginning of the pandemic, and current rescheduling efforts see many loans tenors extended for a further six to 18 months. As such, the full impact of the crisis will only become apparent over the course of 2021.

If the crisis extends and the return to normalcy is further delayed, some financial institutions could potentially face solvency risk, as companies are forced to shut down and households default on their loans. This could push banks and MFIs into survival mode, further restricting credit, which would exacerbate the economic downturn.

Financial institutions have a fiduciary responsibility toward their depositors and other stakeholders to preserve the integrity of their balance sheets, and therefore will most likely err on the side of caution in these adverse circumstances. To mitigate this risk, government-sponsored loan guarantee schemes are essential as they allow financial institutions to keep up the flow of credit, which will be critical to reactivate economies around the region. Argentina, Chile, Colombia, Costa Rica, Honduras, Peru and Uruguay have implemented such guarantee mechanisms with varying conditions and coverage limits, designed to encourage banks to continue lending.

It is important that these types of incentives continue to be implemented across the region, as guarantees will allow financial institutions to leverage the amount of government support with limited resources committed upfront. However, caution will be required to prevent misuse of blanket government support in favor of nonviable borrowers.

The role of public banks in this crisis is also relevant. The possibility of seamlessly implementing public policy through these institutions makes them a vital channel for rapid deployment of resources to sectors where there is more need, such as MSMEs and other vulnerable segments of the population. Several countries are already using their government-owned financial institutions to implement multiple programs. In parallel, private commercial banks and MFIs are well positioned to scale up government sponsored initiatives to deal with the crisis, given their greater capillarity and wider geographical foodprint.

Regulation, supervision, and compliance has improved over the years, as more stringent Basel recommendations have been implemented over time. However, the scope of this crisis is unprecedented, and is yet to be fully felt in loan portfolios. The duration of the crisis, and capacity of FIs to support a return to growth in 2021 will be critical to determining how the next phase plays out.

Although most MFIs are not considered systematically important, a large proportion of the vulnerable population in the region depends upon their services; therefore, it is vital to ensure their survival and sustainability, and their continued role in financial inclusion. The World Economic Outlook published by the IMF points to a slow recovery ahead for LAC, with a 3.6% GDP growth rate in 2021. This, coupled with a so-far-resilient financial system, should place FIs in a position to support the economic recovery in the region.

Authors

Marcelo Paz

Marcelo Paz is a Bolivian national who joined the IDB Group in 2008. He is currently a lead strategy officer, specialized in development diagnosis of the financial and capital markets sectors. Up until 2015 he was in charge of originating and structuring financial transactions that supported the expansion of financial services in LAC through capital markets development, trade finance and financial intermediaries. Marcelo Paz has over 20 years of experience in the banking and financial markets industry, as well as the public sector. Prior to joining the IDB he worked at commercial banking in Bolivia, where he held different positions, such as Credit Risk Manager and International Business Manager, and was a board member at a brokerage firm and a mutual fund. In addition, he worked at the Bolivian Ministry of Finance, and the Bolivian Stock Exchange. Mr. Marcelo Paz holds an MBA in Finance and Investments from George Washington University.

Terence Gallagher

Terence Gallagher is a British national, based in Washington. He began his career as an investment banker at Citigroup, where he spent 9 years supporting emerging market governments and corporates access the international capital markets, working from London, New York and São Paulo. Since 1999, he has dedicated himself to Microfinance, initially working as a consultant for diverse organizations such as Accion International, Development Alternatives Incorporated, and PlaNet Finance. He joined the IFC in 2008 in Rio de Janeiro where he spent 10 years as a Specialist for Micro and Small Enterprise Finance, responsible for investments in Latin America and Sub-Saharan Africa. As of April 2018, Terence moved to Washington to join IDB Invest as head of Financial Inclusion. He has a Masters degrees in Economics from the University of Cambridge, UK.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeAgribusiness

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.