No Data, No Technology: Removing Obstacles from MSMEs' Path to Growth

The growing effort of multinational companies to improve the resilience of their supply chains in the current context has large corporations seeking to outsource from places closer to home, a phenomenon known as “nearshoring.” Before this becomes commonplace, there are obstacles that must be overcome.

The growing effort of multinational companies to improve the resilience of their supply chains in the current context has large corporations seeking to outsource from places closer to home, a phenomenon known as “nearshoring.” Before this becomes commonplace, there are obstacles that must be overcome.

Nearshoring operations represent a unique opportunity for the growth of micro, small, and medium-sized enterprises (MSMEs) in Latin America and the Caribbean (LAC), and have become a strategic priority for the IDB Group to promote economic growth. If we look for the reasons why this has so far only been possible on a limited scale, a key problem is a lack of information.

In a world in which “big data” is an everyday expression, the reality is that LAC is far from being a a land of plentiful digital data. Multinationals usually have neither the information necessary to evaluate potential MSME clients and providers in the region, nor mechanisms to easily capture that data, often due to the lack of formal records; they are thus unlikely to trust a provider they do not know.

Without digital tools to secure and transfer information about your business, a small Chilean or Mexican farmer cannot become part of the production chain of a large supermarket and sell what she grows. A Colombian e-commerce company is going to have a hard time growing if it has no way to collect data on the creditworthiness of its customers. A Brazilian company that needs to transport intermediate goods to be assembled in another country will not be able to rely on an unknown carrier that offers the most competitive cost.

LAC is taking steps in the right direction. For example, the deep-water port of Posorja increased the competitiveness of Ecuador's sea-trade, a key to join regional trade networks, by reducing transit times and increasing its service levels in the loading and unloading of containers, while ensuring the timely application of the proper security protocols.

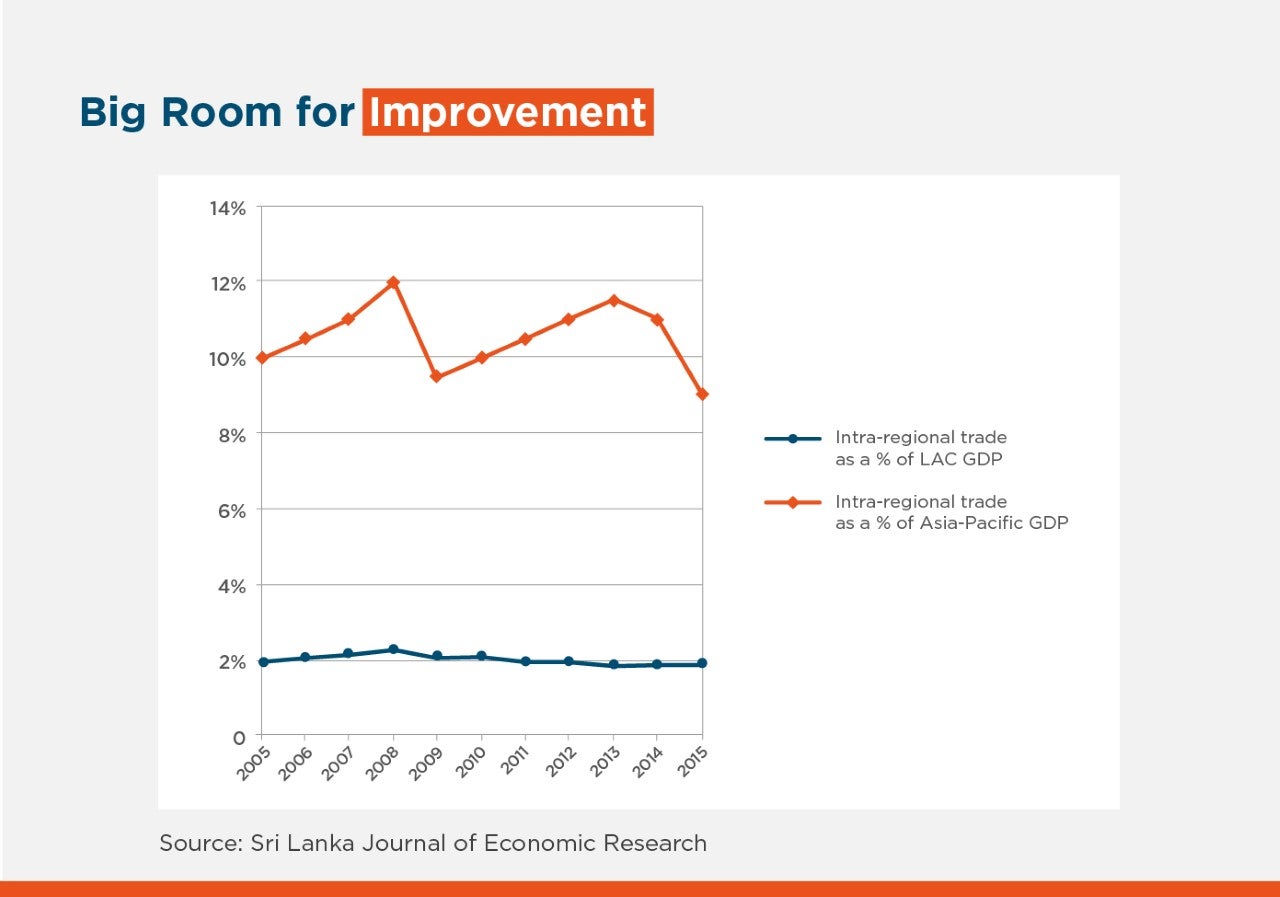

However, if regional trade in LAC is to approach the levels of, for example, Asia-Pacific – where nearshoring has a long history – it is essential that all the agents involved become aware of the need to facilitate the exchange of information and a jump to the digital world.

Large companies, financial institutions and governments must make sufficient technological resources (apps, platforms, etc.) available so that MSMEs are able to capture their information, and promote educational and awareness-raising work in this regard. MSMEs, for their part, must innovate and adapt to new payment mechanisms in order to take full advantage of the digital revolution.

You have to look at the specific obstacles to joining the Fourth Industrial Revolution: a recent study in Argentina shows that almost half of manufacturing firms, mostly SMEs, are technologically lagging behind; in contrast, in Brazil and Uruguay the outlook is more promising, with companies taking effective steps, such as working with banks that offer digital loans and improving their digital infrastructure.

IDB Invest has various financial and non-financial products to support MSMEs and mitigate the traditional barriers that affect their growth and competitiveness, mainly regarding access to financing and information.

Specifically in the field of trade and value chains, IDB Invest's reverse factoring programs offer MSMEs a competitive, efficient and immediate alternative to other types of financing. Through this instrument, IDB Invest seeks the expansion, acceleration and democratization of access to credit for MSMEs that form the backbone of large companies' value chains.

Similarly, IDB Invest has approved an increase in the limit of its program to support foreign trade through banks, the Trade Finance Facilitation Program (TFFP), which this year celebrates its 15th anniversary, from $1.5 billion to $3 billion this year. Under the TFFP, IDB Invest has disbursed several loans specifically geared to financing the import/export activity of MSMEs, through banks in the region.

Authors

Diego Flaiban

Diego leads the Financial Institutions Team for the Southern Cone at IDB Invest, which he joined in 2016. He is responsible for originating and structuring financing operations for financial intermediaries that have an impact on development. Diego has more than 15 years of experience in the IDB Group, where he has led transactions for loans, capital markets and capital investments in the region that promote access to finance, women’s empowerment and climate change mitigation. Before joining the IDB Group, he worked as Senior Consultant and Auditor of Financial Institutions at Arthur Andersen and Deloitte. He previously worked as a loan officer and financial specialist at leading financial institutions in Argentina. Diego earned a graduate certificate in international business from Georgetown University (USA) and an undergraduate degree in public accounting from Universidad de Buenos Aires (Argentina).

Romario Alves Pinto

Romário leads the Trade Supply Chain and Commodity Finance team at IDB Invest, a position he has held since 2017. He develops strategies, mobilizes resources, and implements financial solutions that integrate supply and trade chains to meet clients' needs. Prior to joining IDB Invest, Romário held various roles at Banco Real-ABN Amro, Royal Bank of Scotland, and Bank of America, where he was pivotal in the business development, implementation, and operation of foreign trade and value chain financial products, treasury management, operations, and credit services. With over 43 years of experience, he is a distinguished expert in transactional and structured financial products. Romário holds a master’s degree in business administration (MBA) from the University of London in Madrid, Spain, and is a Certified Public Accountant (CPA) from the Conselho Regional de Contabilidade de Minas Gerais. He also earned a professional degree in Administration and Accounting from Pontifícia Universidade Católica de MG, Brazil.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeFinancial Institutions

Related Posts

How Santander Brasil and Eco Invest Mobilize Private Capital at Scale

IDB Invest provides financing to Banco Santander Brasil to support sustainable agriculture, land restoration efforts, and resilient infrastructure.

S&P’s AAA Rating Validates IDB Invest’s Strength and Strategic Direction

The AAA rating expands the institution's access to a broader investor base, supporting its ability to finance and mobilize private impact investment in Latin America and the Caribbean.

Beyond the Cash Gap: How Reverse Factoring Is Unlocking Growth for MSMEs

An IDB Invest study in Mexico estimates that adopting reverse factoring is associated with a 27% increase in companies' sales.