ESG Factors (1): What's in It for You If You Are in Emerging Markets?

The point of ESG principles is that they should be integrated into company strategy, for the benefit of shareholders and stakeholders, including investors in emerging markets. Non-financial risk disclosure is following the same historical trend as the financial risk report.

Anyone in the know on financial news has heard about environmental, social, and corporate governance (ESG) factors, and how they are promoted at the highest level. But, from emerging markets and in the midst of a pandemic, there is a question to answer: what good are they?

In January this year, the 50th edition of the World Economic Forum (WEF, the so-called “Davos Forum”) renewed its manifesto, advocating a new role for business in the fourth industrial revolution. Klaus Schwab, founder and CEO of the WEF, stated that "capitalism has neglected the fact that a company is a social organism as well as a for-profit entity ... Capitalism is increasingly disconnected from the real economy" .

With these words, Schwab defined the guidelines of a new capitalism in which the purpose of companies is not only to respond to their shareholders, but to society as a whole, particularly to the communities where companies operate and their stakeholders.

Under the premise that companies act as guardians of natural resources for future generations, the need for a transition towards a circular and regenerative economy model is undeniable, a new model that will make it possible to achieve the goals of the 17 Sustainable Development Goals of the UN in the next 10 years.

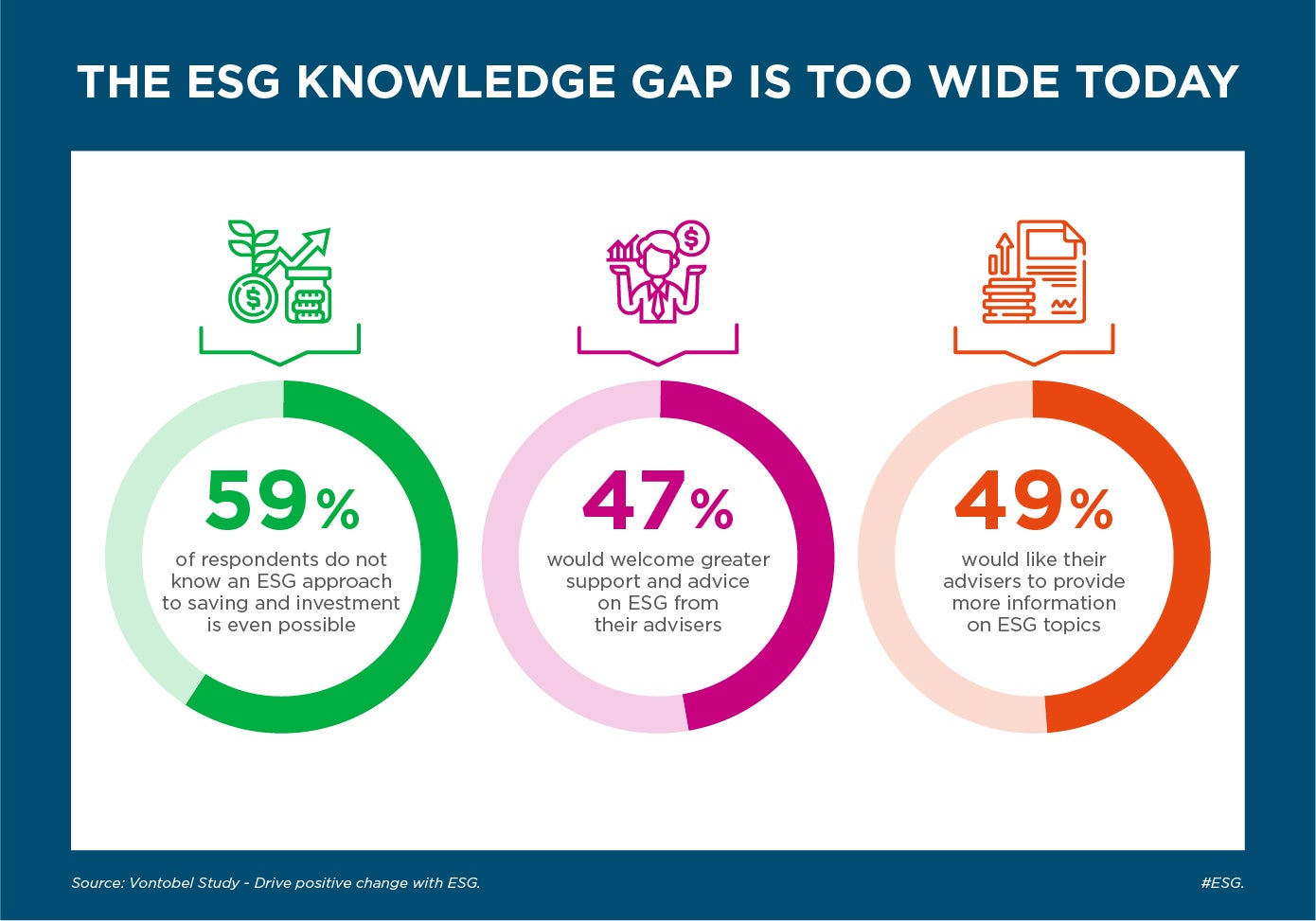

These are certainly well-intentioned initiatives. However, we must examine what's in it for us in Latin America and the Caribbean, the world's region that has been hardest hit by the coronavirus and the ensuing economic crisis. In this article we will focus on the nature of ESG principles, which remain largely unknown even among many investors, while in a future article we will explore how they can be integrated and implemented in all types of companies and institutions.

A key point of the ESG principles is that, by being integrated into your strategy and core business, they can not only increase your rates of return but also be sustainable over time. Similarly, reporting on how these factors are managed must be transparent and periodic, as an essential condition for the satisfaction of all stakeholders: the shareholders of the companies and the communities they serve.

Historically, the way the activities carried out by a company and the events that affect it were recorded and quantified evolved coinciding with the appearance of corporations, towards what we now know as financial accounting.

Financial statements became evidence of a company's ability to generate profits, under independent external review by qualified auditors. Investors' access to verified financial information became an essential condition for the proper functioning of capital markets, and to strengthen investor confidence in issuers.

Over time, the information requirements of investors became more sophisticated, resulting in the need to standardize the financial reporting of corporations globally with accepted accounting principles. A good example was the wave of corporate bond issuance in the US in the late 19th century – triggered by the boom in rail companies – that created a pressing need to meet the demands of European investors. These required access to key credit information on companies, information that could no longer be obtained through communications with business families and banks.

Investors needed independent third parties to provide them with the information on which to base their investment decisions. In this context, the first rating agencies such as Moody’s, S&P, and Fitch emerged, recognized then for the integrity, independence and reliability of their information. Today, regulators in many countries – also in Latin America and the Caribbean – require that fixed income issues be accompanied by a credit rating by a legally recognized credit agency. We are currently observing the same trend and investor requirement to have non-financial information.

At the end of the 20th century, companies began to become aware of their environmental and social responsibility, beyond financials, with the promotion of new financial instruments, guidelines and principles aimed at banks, corporations, issuers and investors, and a multiplicity of initiatives led by multilateral development banks and international organizations. Thus, including ESG factors or risks in decision making and reporting on the process of identification and mitigation of these factors becomes the accepted way of doing business.

In this scenario, environmental risks, related to pollution, biodiversity and climate change; social ones, related to human and labor rights, gender equality, etc; and corporate ones, focused on transparency, internal controls, composition of boards of directors, among others, emerge as a new way of doing business at the corporate level. A way to assess non-financial risks that create opportunities for companies in emerging markets, in the same way that financial risks are assessed.

Authors

Isabel Montojo

Isabel Montojo is an associate in the sustainable finance consulting firm HPL, where she works mainly developing thematic bond frameworks for LAC issuers, and advising on the development of guides and guidelines on sustainable finance for different actors in the capital markets. of ALC. Previously, Isabel worked at the United Nations Global Compact, the UN agency in charge of promoting sustainability within the private sector, and has several years of experience practicing as a US compliance and civil litigation attorney in Spain. Isabel is a lawyer with experience in Corporate Social Responsibility, ESG research and ESG risk assessment and analysis. She has a Law Degree from the Faculty of Law, Complutense University of Madrid and holds an LL.M. in Law and International Justice cum laude from Fordham University School of Law, New York, with a specialization in corporate social responsibility and human rights.

Olga Cantillo

Executive Vice President and General Manager of the Panama Stock Exchange, SA, Olga Cantillo has 30 years of professional experience in the financial industry, specializing in banking and securities markets, and has been in charge of investment and banking operations responsibilities in local and regional financial institutions. She's also Vice President of the Ibero-American Federation of Stock Exchanges (FIAB), Secretary of the Association of Capital Markets of the Americas (AMERCA), Director of the Association of Central Securities Deposits of the Americas (ACSDA), Independent Director of BI Bank Panamá, head of Fundación Calicanto, Founding Associate of the Directors Association of Panama, and member of Renaissance Executive Forums Panama.

Susana del Granado

Susana del Granado is an environmental and social officer at IDB Invest based Panama, responsible for evaluating environmental and social impacts and risks of loans, proposing mitigation measures consistent with international best practices, and supervising project performance. Susana holds a Ph.D. in Natural Resource Management and Environmental Policy from the State University of New York at the School of Environmental Sciences and Forestry (SUNY-ESF) in United States. She also holds a Master of Science from SUNY-ESF and a Master of Public Administration from Syracuse University at the Maxwell School of Citizenship and Public Affairs (United States). She has a degree in biology from the Universidad Mayor de San Andrés in Bolivia. As environmental and social coordinator at the Inter-American Corporation for Infrastructure Financing (CIFI), she has evaluated environmental and social risk in highway, hydroelectric, solar, and port projects in Latin America and the Caribbean. As a senior researcher at the think tank for Advanced Studies in Development (INESAD) she focused on research projects in environmental and ecological economics. She worked as an associate researcher at the Institute of Ecology of La Paz-Bolivia, leading research on adaptation to climate change in Aymara-peasant communities and at the School of Development Studies (CIDES) of the Universidad Mayor de San Andrés, leading historical comparative studies on non-renewable resource management.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeDevelopment Impact

Related Posts

WE Finance Code Colombia: Data and Partnerships to Expand Financing for Women-Led Businesses

Financial sector stakeholders across Colombia are joining forces to expand women entrepreneurs’ access to credit through data, collaboration, and financial solutions tailored to their needs.

Sustainability Week 2026: Choose Your Free Sessions on business innovation and entrepreneurship

Business and knowledge come together at Sustainability Week 2026. Discover our virtual sessions on business innovation and entrepreneurship. Register today.

Corporate Governance: Practical Sessions, from Family Business to AI Oversight

Strong governance is the bridge between business strategy and tangible results. At Sustainability Week 2026 in Barbados, join free training sessions on family governance, AI oversight, and SOE continuity, available online on May 25.