How can Anchor Companies Boost Access to Finance for Their MSME Suppliers?

Increasing access to alternative sources of financing for credit-constrained MSMEs is critical, and supply chain finance has emerged as a viable solution. Reverse factoring—whereby the supplier sells its invoices to a financial intermediary for fast cash, and the buyer guarantees payment of these invoices—shows particular promise.

From the pandemic to the war in Ukraine, the past two and a half years have underscored just how vulnerable global supply chains are to shocks. Consequently, companies seem to be shifting from a focus on supply chain efficiency to resilience to better navigate current and future disruptions. This calls for building the resilience of even the smallest links in the supply chain, and expanding access to supply chain finance for micro, small and medium-sized enterprises (MSMEs) can help.

Within supply chains, MSME suppliers typically have to wait up to 90 days or longer for buyers to pay for the goods delivered. These long cash conversion cycles wouldn’t necessarily be a problem if smaller firms could borrow to finance their working capital in the meantime. However, this isn’t an option for most MSMEs in Latin America and the Caribbean (LAC): despite representing 99% of firms in the region, employing 60% of workers, and accounting for 40% of GDP, MSMEs receive less than 15% of credit provided to enterprises.

This leaves MSME suppliers strapped for cash and stymies their growth potential. Recent evidence from Mexico shows that a lack of short-term financing for working capital may be as much of a constraint to firm performance as a lack of long-term financing for capital investments.

That’s why increasing access to alternative sources of short-term financing for MSMEs is critical. Supply chain finance—which involves collaborative financial solutions agreed among buyers, suppliers, and financial institutions— has emerged as a viable solution to this problem, especially since the 2008 financial crisis. An instrument called reverse factoring shows particular promise in helping suppliers finance their production cycle.

What is reverse factoring?

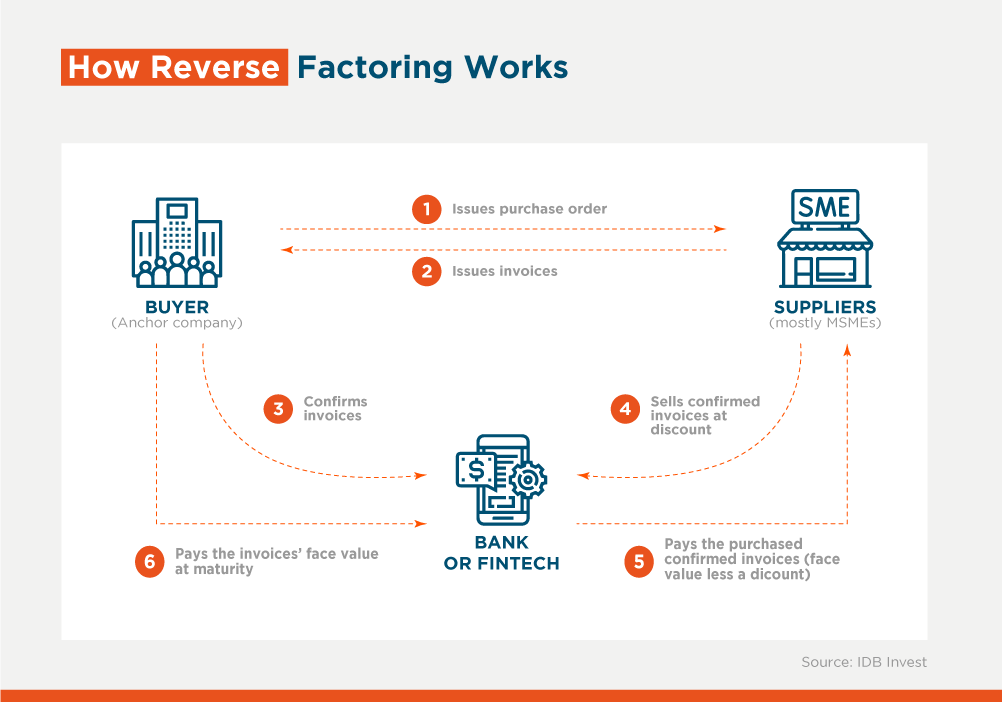

In traditional factoring, in order to get paid more quickly for the goods or services sold to the buyer, the supplier sells its accounts receivable to a financial intermediary to receive fast cash at the cost of a discount – usually equal to an interest rate plus a service fee. Under reverse factoring, the buyer (anchor company) gets involved too by making an irrevocable payment guarantee to the financial intermediary for the supplier’s invoices, thereby increasing the credibility of the payment obligation and reducing risk.

Essentially, reverse factoring allows suppliers to borrow against the value of accounts receivable at lower interest rates because the discount rate is based on the creditworthiness of the buyer (an anchor company with a high credit rating) rather than the supplier (usually MSMEs with high credit risk).

While the use of reverse factoring in LAC is still scarce, it is gaining ground. This is in part due to the digitalization of trade and e-invoices and the emergence of new fintech players helping to further reduce the transaction costs of financing MSMEs, while also increasing speed and transparency. For instance, Brazil, Chile, and Mexico already require e-invoicing and they also lead the way in terms of factoring and reverse factoring uptake in the region.

In a new IDB Invest study, we delve into the evidence surrounding reverse factoring and analyze the benefits and trade-offs for MSMEs in supply chains. These are the top 10 takeaways that emerge from our analysis:

1. Win-win. Reverse factoring can benefit both anchor firms and their suppliers simultaneously.

2. Multiple benefits. The main benefits of reverse factoring may include minimizing market and coordination failures to reduce risks, optimizing working capital within the supply chain, improving trust and commitment between anchor firms and suppliers, and strengthening value chains.

3. Weaker contract enforcement may lead to stronger uptake. For example, reverse factoring may be an attractive alternative in developing countries where traditional bank credit is limited due to difficulties in drawing up debt contracts, collateral enforcement, and collecting in the case of default.

4. Greater working capital needs and more MSMEs means more reverse factoring. Reverse factoring is more common in more working capital-intensive sectors and among suppliers that are MSMEs and/or more credit constrained.

5. Buyers are influencers. Adoption of reverse factoring is greater and faster if the buyer has high procurement volumes, more influence over its suppliers, and operates in an industry with longer payment terms.

6. See it to believe it. Uptake of reverse factoring by suppliers may be slow at first but increases dramatically when companies observe the benefits obtained by early adopters.

7. Context matters. Suppliers use and benefit more from reverse factoring in the context of: (a) larger interest rate spreads in external financing and/or more constrained access to credit compared to the anchor buyer; (b) more aggressive working capital policies; (c) higher demand volatility for their products or services; and (d) higher risk-free interest rates.

8. Be careful of payment extensions. The extension of payment terms by the buyer while implementing a reverse factoring scheme induces a trade-off for the supplier and therefore needs to be carefully assessed.

9. Payment extensions may work in some cases. Payment extensions in the context of reverse factoring are less harmful for suppliers in industries which already have long payment periods and when their buyers have good credit ratings and high procurement volumes.

10. Build the evidence base. While many studies highlight the potential of reverse factoring for financing MSMEs, more rigorous data analysis on the use and impact of this approach is needed both for advancing the academic and managerial literature on this topic and for designing better-targeted public and private interventions.

For more details, see Reverse Factoring for MSMEs: A Financial Tool for Supply Chain Development?

Authors

Gabriela Aparicio

Gabriela Aparicio is a Development Effectiveness Officer in the Development Effectiveness Division (DVF) of IDB Invest, where she works in the structuring, supervision, and evaluation of projects in the manufacturing, tourism, and agroindustry sectors, as well as in the production of knowledge products. Prior to joining IDB Invest she worked as a consultant in the Office of Strategic Planning and Development Effectiveness, and the Research Department of the Interamerican Development Bank (IDB), and as a Junior Professional Associate at the World Bank. She has a PhD in Economics from the George Washington University.

Lucas Figal Garone

Lucas Figal Garone is Lead Economist of Development Impact for Latin America and the Caribbean at IDB Invest, Inter-American Development Bank (IDB).

He has more than 15 years of experience leading the design, monitoring, and evaluation of public and private sector development projects with the aim of maximizing their impact. He also leads economic analyses, studies, impact assessments, and testing of innovative solutions for the generation and dissemination of knowledge linked to the operational experience of IDB Invest, its clients, and the public-private sector in the region.

Previously, he worked in the Competitiveness, Technology, and Innovation Division, and the Strategic Planning and Development Effectiveness Division at the Inter-American Development Bank (IDB) in Washington, D.C.

Lucas is also Visiting Professor in the Economics Department at the Universidad de San Andrés (UdeSA) and coordinator of the SIDPA productive development initiative.

His areas of expertise and interest include development economics, productive development, impact evaluation, and applied economics. His recent research includes publications in World Development, Regional Science and Urban Economics, Research Policy, The Journal of Development Studies, Small Business Economics, Research in Economics, Journal of Development Effectiveness, Emerging Markets Finance and Trade, IDB WP Series, IDB Invest Development through the Private Sector Series, and chapters in several books.

He holds a PhD in Economics from UdeSA, where he also obtained his Master's degree in Economics, after completing his Bachelor's degree in Economics at the University of Buenos Aires (UBA).

Alba Quilez Llopis

Alba is an Investment Officer in the Financial Products and Services Division of IDB Invest. As a member of the Trade and Supply Chain Finance team, she is responsible for providing trade and supply chain solutions to IDB Invest clients, including private sector companies and financial intermediaries. These solutions consist in import/export loans and guarantees, receivables discounting, payables finance, among other instruments. Alba has worked for the IDB Group since 2010, holding different positions as trade finance specialist. Before joining the IDB Group, Alba worked as an investment analyst in the Trade Commission of Spain in New York and as a strategic consultant in Analistas Financieros Internacionales, a leading consulting firm in Madrid. She started her career in London, where she worked for CAM bank. Alba holds an MBA from IE Business School with a specialization in corporate finance and several certificates as trade finance specialist.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

Subscribe{{ raw_arguments.field_category_target_id }}

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.