Three Ways to Protect the Sustainability-Linked Bond Market

The risks involved in sustainability-liked bonds often focus on insufficiently robust and ambitious targets and KPIs, improperly crafted incentives and structural loopholes. All these can be alleviated with better monitoring of issuers.

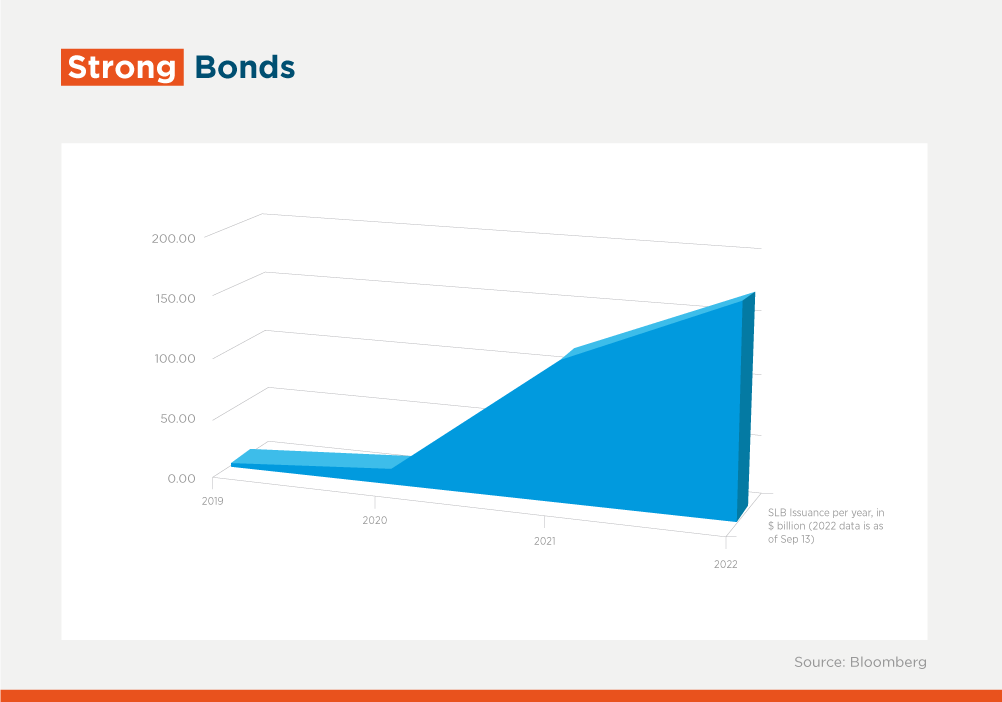

As Sustainability-Linked Bonds, or SLBs, have become a popular instrument for issuers and investors, green-washing is commonly cited as a concern. But it’s far from the only risk investors need to consider.

Like we explained in a previous post, SLBs are forward-looking instruments where issuers predetermine sustainability-performance targets and key performance indicators (KPIs) to measure against over time. In the vast majority of publicly placed SLBs, the securities’ yield is the structural feature that goes up if these targets are not met, creating a financial incentive for corporate management to pursue those goals.

SLBs provide issuers with much leeway for the use of proceeds and market participants are getting a better understanding of their risks and rewards, as well as how they can be “gamed”. The risks involved in these issues can be grouped in three main categories: insufficiently robust and ambitious targets and KPIs; improperly crafted incentives; and structural loopholes:

(A) Insufficiently Robust and Ambitious Targets and KPIs

The targets and KPIs used for many of the SLBs have been strongly criticized by practitioners for not always being sufficiently ambitious, aspirational and science based. These objections were partially addressed by the International Capital Markets Association (ICMA) during its Annual General Meeting earlier this year, when it published a KPI registry covering over 20 sectors, with the goal of providing market participants additional tools to better design and assess the materiality of KPIs, thus enhancing the SLB market transparency and integrity.

The registry supports the classification of KPIs as core or secondary. Core KPIs are qualified as sufficiently material, mature and holistic as to allow their use on a standalone basis, while secondary KPIs are subject to relevant limitations and should not be used on a standalone basis. Few KPIs are sufficiently robust to be considered as core for any given sector and SLBs should always incorporate at least one of them.

Investors can – and should – also demand additional perspective from reputable second party opinion providers who can also assist them in evaluating the quality and ambitions of baseline targets and KPIs. The market would also benefit from clearer guidelines for sovereign SPTs and KPIs in SLBs.

(B) Improperly Crafted Incentives

At the core of the SLB market are the incentives for corporate management to pursue targets. To date, the vast majority of outstanding SLBs has incorporated an incentive mechanism in the form of a coupon step-up in case of issuers’ failure to meet their pre-agreed SPTs by the verification date. This structure could represent a potential moral hazard to investors, who would arguably benefit from improved yields based on issuers’ failure to meet their KPIs. While this is a valid concern, this reputational risk can be mitigated by investment firms creating and adopting a robust impact framework setting forth an in-depth evaluation of the SLB instruments (including KPIs and SPTs), their alignment with their own institutional environmental, social and governance (ESG) strategy, as well as other risks inherent to the sectors and individual issuers.

Other creative solutions to remedy this potential moral hazard have emerged. In October, the Republic of Uruguay made history by launching the world’s first-ever SLB with a two-way coupon-step structure (i.e. up, down or no change), driven by the Republic’s performance in connection with reductions in greenhouse gas emissions and preservation of natural forests, as a proxy for the country’s carbon capture capacity.

Despite persistent on-going volatility in capital markets, investor demand was strong, and the deal priced successfully. The Inter-American Development Bank and the United Nations Development Programme provided technical assistance and support for Uruguay’s landmark Sustainability Framework. This is the first SLB bond that is fully consistent with the Emerging Markets Investors Alliance’s (EMIA) Enhanced Labelled Bond Principles, encouraging an elevated level of transparency and more stringent terms.

Another example of a creative solution conceived by the market was Etihad Airways’ 2020 issuance of a 5-year SLB in which the penalty for not meeting the one SPT in the instrument (a 17.8% reduction in the carbon intensity of passenger fleet by 2024) was the commitment by the issuer to purchase carbon offsets of a corresponding amount.

The magnitude of the financial incentive is also key to ensure market integrity. In a recent paper analyzing SLBs in its database, Fitch found almost no correlation between issuers’ credit rating and the applicable step-up, the ambition of the targets set or the cost required to achieve them. This brings a potential limitation as borrowers may seek to benefit from the “halo effect” of issuing a SLB, without material consequences in case of failure to meet targets.

The solution to this is to ensure that the potential step-up is actually material for the issuer’s financial conditions and credit profile, creating meaningful incentives for corporate management to set targets as a strategic priority.

(C) Structural Loopholes

Structural loopholes have occasionally been exploited by issuers to circumvent the consequences of not meeting the SPTs. For example, some borrowers have set the targets’ review date too close to the instruments maturity to minimize negative effects of a coupon step-up. Issuers should adopt (and investors should demand) more stringent requirements such as the one set by ELBP 14, demanding that trigger events should be set no later than midway between the issuance date and either the maturity date or call date, whichever comes earlier.

Voluntary call optionality has also been used by issuers to dodge the potential step-up in coupon. If the issuer is behind schedule to meet targets, it could theoretically exercise a voluntary call option prior to the verification date. One way to avoid this risk is to include a contractual provision requiring that any voluntary call option exercised prior to the verification date includes the step-up in coupon unless targets have been met in advance.

“KPI restatement mechanisms” remain another controversial topic in SLBs, as they could give issuers a way out of paying step-up coupons if they miss KPI targets under certain circumstances. For example, some issuers set major corporate events such as acquisitions or disposals as hypotheses to unilaterally amend targets, which may undermine the integrity of the instrument. A possible remedy for this is to limit such hypothesis as much as possible, or at least to subject any changes to SPTs and remedies to the approval of bondholders.

In summary, SLBs have grown to be an important instrument in the Debt Capital Markets and have the potential to reshape the entire sustainable debt market industry. However, the flexibility provided to issuers requires practitioners to design the instruments and incentives responsibly, at the risk of putting the integrity of this market in question, particularly for issuers in high-risk sectors or in EM countries.

Investors in these instruments should establish a robust ESG framework incorporating in-depth analysis of both sector and issuers’ ESG risks. Use-of-proceeds bonds remain a solid alternative for higher risk industries and issuers not yet developed enough to commit to a serious institutional ESG strategy, and for investors first getting involved in ESG investing, since the projects eligible to receive funds are specified at issue and the associated outcomes can be more easily assessed, benchmarked and reported. SLBs represent a powerful, flexible tool for borrowers and investors with a robust ESG framework in place to pursue ambitious and relevant goals towards required change. Thought leaders such IDB Invest and organizations such as EMIA, which enables institutional investors and help shape the industry, have the responsibility to continue to advocate for the adoption of best practices and knowledge sharing, raising awareness and contributing to the continued advancement of this market.

Authors

Nadine Cavosoglu

Nadine Cavusoglu is Head of Private Sector Programs at EMIA

Barbara Oldani

Barbara Oldani is Sovereign Decarbonization Program Director and Labeled Bonds Lead at EMIA

Carole Sanz-Paris

Carole Sanz-Paris leads the debt capital markets team at IDB Invest. She is a specialist in fixed income, structured finance transaction execution, sale-side research, and credit analysis. She defines herself as passionate about investing with social impact. Carole has more than 20 years of experience in global capital markets; she has been responsible for the structuring, execution and placement of many complex financial structures, including securitizations. She has published extensively on the relative value of fixed income products and credit analysis, having developed her interest in social responsibility and impact investing while earning her Executive MBA from Oxford University.

Andre Almeida Pamponet Moura

Andre Almeida Pamponet Moura is a senior Debt Capital Markets and Structured Finance (DCM & SF) professional with dual expertise in Finance and Law. With over 15 years of experience in business development, structuring of innovative financial transactions, leadership in complex projects, and successful client relationship management, Andre has ample exposure to several domestic and international financial markets across Latam and EMEA. Andre is certified in ESG Investing by the CFA Institute and has hands-on expertise in Environmental/Social/Governance (ESG) topics, impact investing and development finance. Andre holds a Bachelor of Law Degree from the University of São Paulo (Brazil) and an MBA Degree from INSEAD (France/Singapore).

Diana Carrillo Sosa

Diana Carrillo Sosa is an Analyst in Debt Capital Markets and Structured Finance at IDB Invest. Before joining IDB Invest she worked in private equity, venture capital, and impact investing. She defines her professional goal as developing and supporting solutions that contribute to climate change mitigation and social justice. Diana earned a master’s degree in psychology of Economic Life from the London School of Economics and Political Science and has a undergraduate degree in finance from the Instituto Tecnológico Autónomo de México.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeClimate change

Related Posts

2024, the Year the World Turned Its Eyes to the Amazon Region

The "lungs of the planet," was one of the major topics of the past twelve months. Despite significant challenges, the region has much to offer regarding global solutions that drive sustainable development. Here is a selection of blogs we published on the topic.

Addressing Climate Change Through Improved Business Continuity

The increasing impact of climate change on the Caribbean, emphasizes the need for effective business continuity management to mitigate disruptions.

Assessing Climate Risks Is Vital for Companies, the Economy and the Environment

Although each company’s adaptation strategies must be tailored to its unique circumstances, ignoring climate change is never wise. Conducting a professional assessment is the best approach to making informed decisions.