Fighting Greenwashing & Other Risks in the Sustainability-Linked Bond Market

Sustainability-linked bonds provide issuers with much leeway for the use of proceeds and market participants are getting a better understanding of their risks and rewards, as well as how they can be “gamed”. Green-washing is only one of several risks looming.

Sustainability-Linked Bonds, or SLBs, are a great way to support issuers sustainability strategy without earmarking the capital raised for specific goals. As this market matures, “green-washing” and other risks are being identified and dealt with by market participants.

Since the first green bond issuance in 2008, the labelled bond market has matured, with green, social and sustainability issuances galore. These are instruments in which the use of proceeds is predefined and applied to one or more specific green, social and/or sustainable project.

However, the market demanded more flexibility considering that some issuers did not have a particular pool of projects that met the requirements to be classified as such, nor met the minimum principal requirement for public issuances. Enter SLBs, defined by the International Capital Markets Association as “any type of bond instrument for which the financial and/or structural characteristics can vary depending on whether the issuer achieves predefined Sustainability/ESG objectives”.

By design, SLBs are forward-looking instruments where issuers predetermine sustainability-performance targets and key performance indicators to measure against over time, including financial penalties in case the targets are not met after some pre-agreed timing. In the vast majority of publicly placed SLBs, the securities’ yield is the structural feature that changes, with a step-up in the coupon of the bonds creating a financial incentive for management to pursue those goals.

Unlike the use-of-proceeds bonds (such as green, social, sustainable, gender, etc.), issuers of SLBs normally have no restrictions regarding the deployment of the funds raised, with the generic “general corporate purposes” (or “general budget purpose” in the case of sovereign issuers) bucket being common.

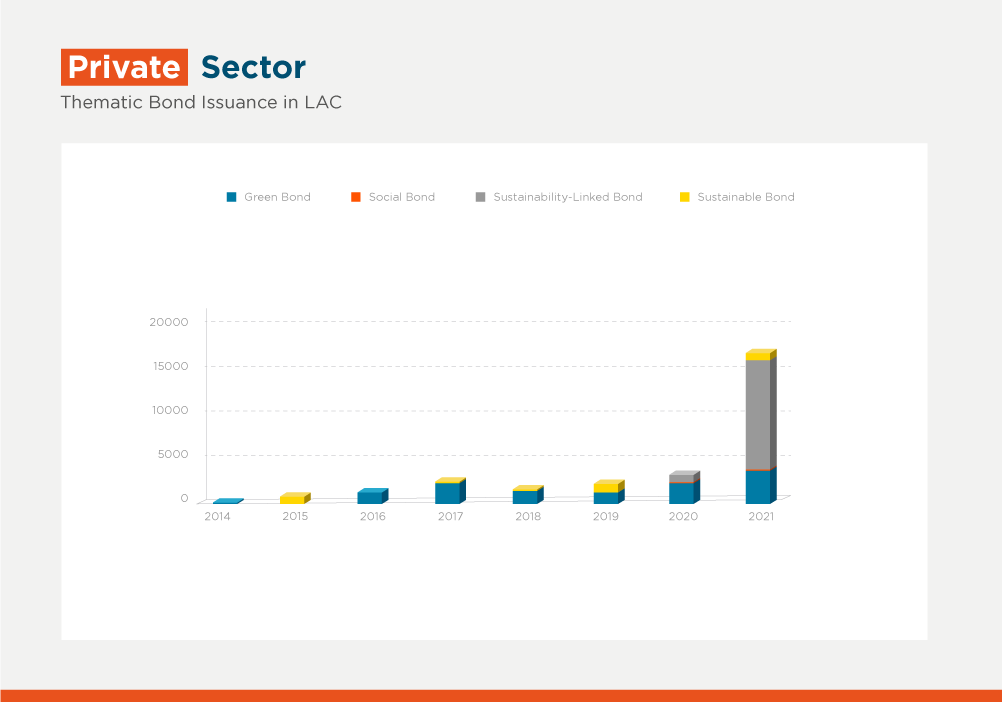

For this reason, SLBs are increasingly popular among issuers who appreciate the flexibility of use-of-proceeds. As a result, the SLB market has witnessed a strong expansion in recent years, reaching US$135 billion in outstanding securities in 2021, with an additional cumulative US$46.6 billion during the first half of 2022 according to the Climate Bond Initiative.

While an important tool to foster desired results, incentives can also bring unintended negative consequences if poorly crafted. As this market continues to mature, practitioners are progressively understanding these instruments, their benefits, risks, and rewards, as well as how they can be “gamed”.

To address potential shortcomings, the Emerging Markets Investors Alliance (“EMIA”) has published its second edition of the’ Enhanced Labeled Bond Principles to promote the development of labelled bonds and SLBs that can make a meaningful contribution towards improved environmental, social, and governance (ESG) outcomes in these instruments. Entities like IDB Invest also strive to incorporate in its investments market best practices and mitigants to address potential SLB shortcomings and establishing good benchmarks.

Beyond the well-known reputational risk of “green-washing” – the act of providing investors with misleading or outright false information about environmental impact of a company’s products or financial instruments – other points of attention for the integrity of the SLB market can be grouped in three main areas: (a) Insufficiently Robust and Ambitious Targets and KPIs; (b) Improperly Crafted Incentives; and (c) Structural Loopholes.

This is the first post of a series of two collaborations between IDB Invest and the Emerging Markets Investors Alliance. We will address those risks and possible mitigants in our next blogpost. Stay tuned!

Authors

Nadine Cavosoglu

Nadine Cavusoglu is Head of Private Sector Programs at EMIA

Barbara Oldani

Barbara Oldani is Sovereign Decarbonization Program Director and Labeled Bonds Lead at EMIA

Carole Sanz-Paris

Carole Sanz-Paris leads the debt capital markets team at IDB Invest. She is a specialist in fixed income, structured finance transaction execution, sale-side research, and credit analysis. She defines herself as passionate about investing with social impact. Carole has more than 20 years of experience in global capital markets; she has been responsible for the structuring, execution and placement of many complex financial structures, including securitizations. She has published extensively on the relative value of fixed income products and credit analysis, having developed her interest in social responsibility and impact investing while earning her Executive MBA from Oxford University.

Andre Almeida Pamponet Moura

Andre Almeida Pamponet Moura is a senior Debt Capital Markets and Structured Finance (DCM & SF) professional with dual expertise in Finance and Law. With over 15 years of experience in business development, structuring of innovative financial transactions, leadership in complex projects, and successful client relationship management, Andre has ample exposure to several domestic and international financial markets across Latam and EMEA. Andre is certified in ESG Investing by the CFA Institute and has hands-on expertise in Environmental/Social/Governance (ESG) topics, impact investing and development finance. Andre holds a Bachelor of Law Degree from the University of São Paulo (Brazil) and an MBA Degree from INSEAD (France/Singapore).

Diana Carrillo Sosa

Diana Carrillo Sosa is an Analyst in Debt Capital Markets and Structured Finance at IDB Invest. Before joining IDB Invest she worked in private equity, venture capital, and impact investing. She defines her professional goal as developing and supporting solutions that contribute to climate change mitigation and social justice. Diana earned a master’s degree in psychology of Economic Life from the London School of Economics and Political Science and has a undergraduate degree in finance from the Instituto Tecnológico Autónomo de México.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeAgribusiness

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.