Can Digital Credit Boost E-commerce among MSMEs?

Reaping the rewards of e-commerce is a challenge for many MSMEs. The solution may lie in the so-called “digital credit” offered by fintech companies within commercial platforms that bypass traditional banks.

One of the biggest challenges facing Latin American and Caribbean (LAC) economies is the incorporation of micro, small and medium enterprises (MSMEs) into e-commerce. So-called “digital credit” may offer a solution.

While 99% of firms in the region are MSMEs, which generate 60% of jobs and 40% of GDP, they receive less than 15% of business credit and only 1% participate in e-commerce.

The economic impact of the pandemic has heightened these problems. Most of these businesses faced stark drops in demand for their products, many were forced to halt operations, and despite public policies implemented to alleviate this situation, their access to credit was also affected. Many MSMEs did not make it.

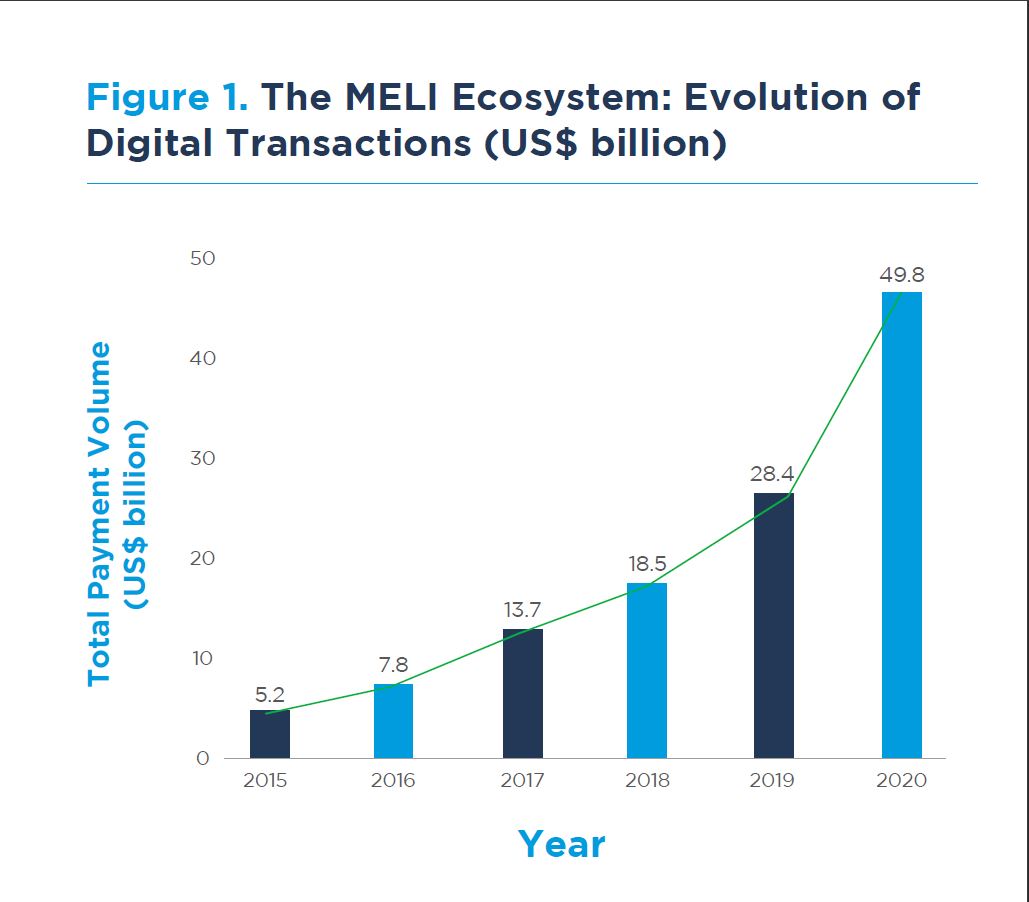

At the same time, the pandemic has also created new opportunities, leading many companies to seek new online sales channels and use e-commerce to survive. While the number of digital transactions through Mercado Libre (MELI), the region’s main e-commerce platform, had already been growing significantly pre-pandemic, they reached US$50 billion in 2020, a 75% increase over 2019.

For consumers, e-commerce can increase competition, facilitate price comparisons, expand the variety of products available, and save time. Businesses can also benefit from reduced costs, greater efficiency, and access to new clients. Additionally, digital payments allow for greater traceability of business operations, making monetary transactions more secure, reducing informality, and facilitating tax collection.

To promote greater uptake of e-commerce among MSMEs, it is important to understand the barriers that hinder their participation in the first place. These include persistent digital gap problems (lack of internet connectivity, computers, and human resources with digital skills), informality, limited financial literacy, and underdeveloped logistics channels, among others. Insufficient access to financing can also make it difficult for MSMEs to “go digital” and reduce their capacity to grow online sales.

The Case of Mercado Crédito in Argentina

IDB Invest, together with MELI, carried out a study to understand how access to financing can affect the level of MSME participation in e-commerce. MELI provides an ideal setting for exploring this question since it offers credit to companies who operate within its ecosystem through Mercado Crédito.

Mercado Crédito is an innovative platform that offers consumer loans and working capital loans to MSMEs that sell through MELI or process their sales through Mercado Pago (MELI’s payment platform). It aims to make access to financing simple, flexible, and tailored to clients’ needs, reaching people and businesses that are underserved or unserved by the traditional financial system.

The online loan application is user-friendly: it does not require additional documentation and loans are granted instantaneously. Loan terms are flexible, as the seller can select the desired credit amount and repayment schedule, which will be deducted from their future sales on the platform.

As of the end of 2020, Mercado Crédito had provided 3.5 million loans totaling over $2.7 billion to more than 1 million MSMEs in Argentina, Brazil, and Mexico. They are mostly working capital loans with an average size of $450 and repayment period of 11 months.

Sales Increase for Firms that Received Credit

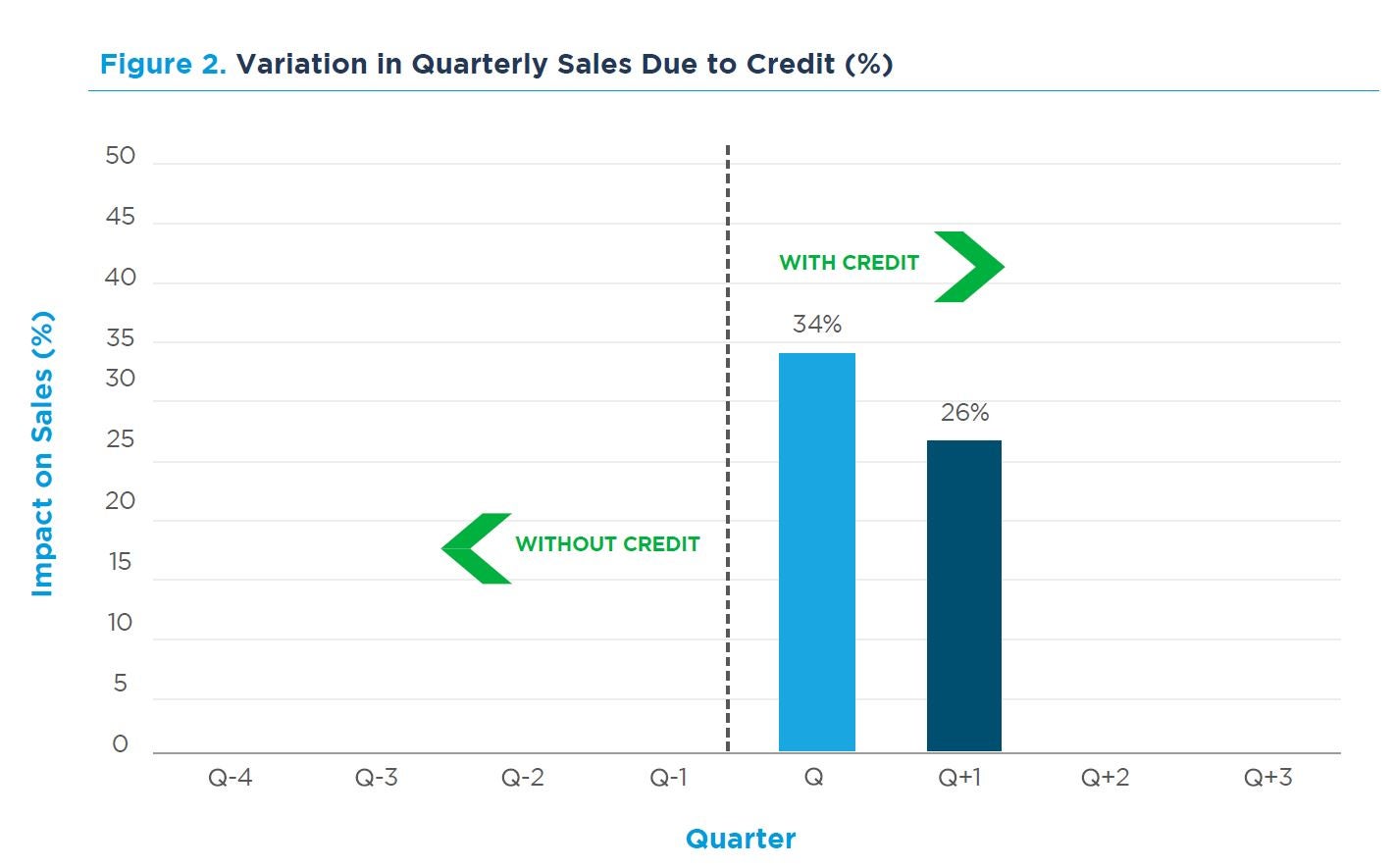

Companies that did receive the credit increased their quarterly sales through MELI platforms for six months—by 34% on average during the first quarter and by 26% in the following quarter—compared to similar companies that did not receive the credit. In dollar terms, the average seller who received the credit sold about AR$376,000 more (nearly $4,300) over a six-month period than they would have sold without it.

This effect was also clear in the months following the implementation of pandemic lockdowns and social distancing measures in Argentina: the quarterly sales of MSMEs receiving the credit in the second quarter of 2020 within the MELI ecosystem were 55% higher than those that did not receive credit, and 36% higher in the following quarter.

These results show that the effect of credit on MSME digital sales within the MELI ecosystem lasts up to six months, with firms then returning to their average sales levels. This is in line with the type of short-term working capital loans offered by Mercado Crédito.

Leveraging a fintech company and an e-commerce platform can help boost MSME digital sales within that ecosystem. Nonetheless, it remains to be seen how more MSMEs can pursue a digital transformation to reap the rewards of e-commerce. The challenges are big, but so are the benefits, especially in a post-pandemic world where e-commerce will likely be here to stay.

(Gonzalo Arauz contributed to this post)

Authors

María Laura Lanzalot

María Laura Lanzalot is the Development Effectiveness Officer of IDB Invest in Argentina. María Laura supports the identification, design, monitoring and evaluation of projects and investments in order to maximize their impact on economic, social and environmental development, with a focus on projects with financial institutions. Additionally, she contributes in the implementation of economic analysis, impact evaluations and testing of innovative solutions. Previously, she worked in the Department of Development Effectiveness in Washington DC. Her areas of interest are economic development, financial inclusion and applied economics. She has a master's degree in economics from the Universidad de San Andrés (UdeSA) and a bachelor's degree in economics from the University of Buenos Aires (UBA).

Rodolfo Stucchi

Rodolfo Stucchi is Director of Development Impact at IDB Invest. His areas of expertise include development economics, public policy evaluation, and macroeconomics. Rodolfo has extensive experience in portfolio monitoring and management, ex-ante and ex-post economic analysis of public and private sector projects, monitoring and evaluation, impact evaluations, and macroeconomics. Previously, he was Head of Development Impact for the Andean Region and the Southern Cone and Head of Monitoring and Evaluation both at IDB Invest. He also was Senior Economist at the Inter-American Development Bank, consultant for the Inter-American Development Bank and The World Bank, and Economist for the Government of the Province of Córdoba in Argentina. Rodolfo has published numerous papers in peer-reviewed journals, such as the Journal of Development Economics, Journal of Development Studies, Journal of Macroeconomics, The World Bank Economic Review, and Economia, among others. His research focuses on topics related to productivity, employment, innovation, trade, and access to credit. He was also Visiting Professor at Universidad de San Andrés (Argentina), Universidad Católica Boliviana San Pablo (Bolivia), Universidad de Chile (Chile), and Georg-August-Universität-Göttingen (Germany). Rodolfo holds a PhD in Economics from Universidad Carlos III de Madrid (Spain) and a BSc in Economics from Universidad Nacional de Cordoba (Argentina).

Lucas Figal Garone

Lucas Figal Garone is Lead Economist of Development Impact for Latin America and the Caribbean at IDB Invest, Inter-American Development Bank (IDB).

He has more than 15 years of experience leading the design, monitoring, and evaluation of public and private sector development projects with the aim of maximizing their impact. He also leads economic analyses, studies, impact assessments, and testing of innovative solutions for the generation and dissemination of knowledge linked to the operational experience of IDB Invest, its clients, and the public-private sector in the region.

Previously, he worked in the Competitiveness, Technology, and Innovation Division, and the Strategic Planning and Development Effectiveness Division at the Inter-American Development Bank (IDB) in Washington, D.C.

Lucas is also Visiting Professor in the Economics Department at the Universidad de San Andrés (UdeSA) and coordinator of the SIDPA productive development initiative.

His areas of expertise and interest include development economics, productive development, impact evaluation, and applied economics. His recent research includes publications in World Development, Regional Science and Urban Economics, Research Policy, The Journal of Development Studies, Small Business Economics, Research in Economics, Journal of Development Effectiveness, Emerging Markets Finance and Trade, IDB WP Series, IDB Invest Development through the Private Sector Series, and chapters in several books.

He holds a PhD in Economics from UdeSA, where he also obtained his Master's degree in Economics, after completing his Bachelor's degree in Economics at the University of Buenos Aires (UBA).

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeFinancial Institutions

Related Posts

How Santander Brasil and Eco Invest Mobilize Private Capital at Scale

IDB Invest provides financing to Banco Santander Brasil to support sustainable agriculture, land restoration efforts, and resilient infrastructure.

S&P’s AAA Rating Validates IDB Invest’s Strength and Strategic Direction

The AAA rating expands the institution's access to a broader investor base, supporting its ability to finance and mobilize private impact investment in Latin America and the Caribbean.

Beyond the Cash Gap: How Reverse Factoring Is Unlocking Growth for MSMEs

An IDB Invest study in Mexico estimates that adopting reverse factoring is associated with a 27% increase in companies' sales.