Six Reasons Why Your Company Should Consider Mezzanine Debt

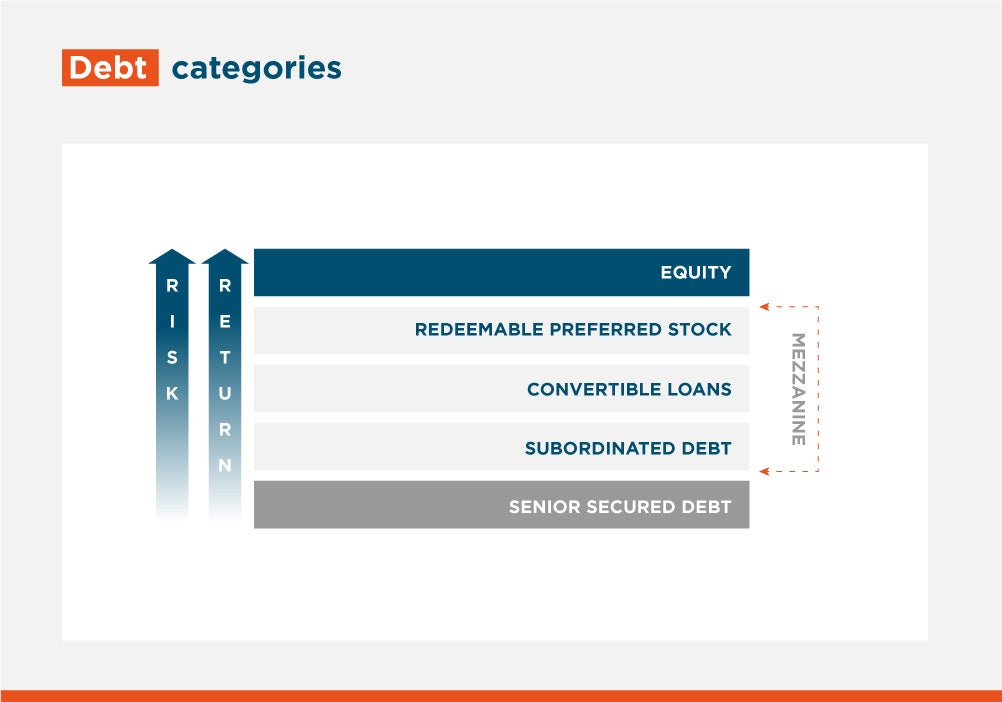

Mezzanine instruments fit right between traditional senior secured debt and old-fashioned equity, both in terms of risk and returns. If structured properly, they may do wonders for companies, especially those struggling to secure financing in the current economic context.

Companies looking to raise funds from traditional financial institutions typically look at either debt or equity alternatives, and naturally end up choosing one at either end of the spectrum. However, there is the “in-between” option of mezzanine financing, which continues to evolve and may be a more useful alternative to fundraising.

A mezzanine instrument fits right between traditional senior secured debt and old-fashioned equity, and, at the same time, it can borrow elements from both to adapt to any scenario. Additionally, its yield potential rests right between these two boundaries and, if structured adequately, will fit properly in the capital stack of the company.

Historically, mezzanine debt was associated with high yielding, less flexible and complex instruments, normally tied to high leverage, event-specific and sometimes even distressed scenarios. When the product was originated several decades ago, mezzanine facilities often carried strict terms and allowed limited flexibility with respect to repayments and compensation options.

More recently, mezzanine debt evolved to become a very useful tool to provide risk capital when other sources of funding are not available. Within emerging markets, and particularly in Latin America and the Caribbean (LAC), access to liquidity, especially through public listings, can be challenging. Raising risk capital through facilities like mezzanine with self-liquidating features allows companies access to this creative form of funding.

Here are six reasons why your company should consider raising mezzanine debt:

- No assets, pledged assets: Businesses with asset-lite models, or which already have some assets pledged towards other debts, can access mezzanine and consider structures with second liens on such assets – and also consider share pledges as alternative collateral.

- Need capital, have cashflow and do not want dilution: This applies particularly to family-owned businesses or companies which already have an equity sponsor that have decent cashflow and want risk capital without (all) the dilution. Mezzanine does not necessarily eliminate all dilution as various structures may carry warrants, equity kickers, etc. but, if structured adequately, it will not provide as much dilution as plain vanilla equity.

- Too much debt on my hands: Certain high-leverage situations can entertain adding an additional layer of mezzanine debt if the business can cover the servicing of all debts. Mezzanine in these circumstances will commonly switch to a payment-in-kind, postpone, and accumulate payments in events in which coverage becomes tight.

- Under pressure (get me out): Mezzanine debt can also be utilized to fund liquidity for departing shareholders however, investors might not want their funding to be utilized for paying off shareholders, but rather to grow the business.

- Refinancing satisfaction: more traditionally, mezzanine can be utilized to refinance near term maturities or inadequately structured high yield debt.

- Bridge over troubled water: equity like mezzanine can be used as temporary financing intended to cover cash deficits up until a new equity round is secured. Usually, the mezzanine can be structured as a convertible security and will contain certain features such as coupon, discount in conversion price, etc.

In emerging markets, mezzanine debt is a natural fit for small and medium enterprises (SMEs) as traditional senior loan structures can be much less flexible and cumbersome while equity funding is reserved for more established, larger players and is considerably more expensive and dilutive.

IDB Invest has developed a suite of mezzanine products to expand the availability of equity-like and debt-like capital in the region combining financial with non-financial solutions to ensure the investments maximize value. Flexibility in product construction allows targeting of industries where plain vanilla instruments are not suitable, while leveraging partnerships to mobilize resources, achieving impact through the entire region.

Over the course of the past few years, IDB Invest has structured various tailor-made facilities to provide mezzanine-like capital to regional clients under very special and unique circumstances. That includes a facility structured to support Cabify’s growth strategy with enough flexibility to support the company’s expansion plan throughout the region. Cabify is a large regional player in the ride-hailing segment which had raised significant equity but was not yet considered by traditional lenders to raise conventional debt.

IDB Invest also promoted the reactivation of tourism in the region by supporting Selina, a large regional player in the sustainable tourism sector, as it managed through the turbulent waters of the Covid 19 pandemic, with a facility that adapted to its cash flow, as its operations returned to historical levels.

In addition, it reinforced the potential of e-commerce with the financing of Gaia, a large Mexican player in the e-commerce furniture sector with a convertible instrument to provide a strong bridge, as the company continues its growth path and can comfortably raise a new equity round down the road.

Having a wide array of competitive products, while pushing out IDB Invest’s important agenda of sustainable development, is key. In the context of the COVID-19, IDB Invest has provided support to core segments focusing on issuers that have historical profitable foundations and strong equity bases but, in the current environment of more constrained economic outlooks, have been unable to attract capital at acceptable terms.

Authors

Mónica Salazar

Mónica is an Investment Management Officer in the Equity & Mezzanine Finance Team at IDB Invest, which she joined in 2017. She is responsible of sourcing, selecting, originating, structuring, closing and supporting the supervision of the equity and mezzanine transactions (including venture capital), across all sectors of IDB Invest. Before joining the IDB Group, she worked as an Investment Analyst in the Private Equity Division of the Development Bank of Latin America (CAF, in Spanish), performing financial analysis and portfolio valuations of direct investments and private equity funds (approx. $600 million of AUM). She also has experience in project assessment in the financial and energy sectors in Venezuela. Mónica earned a master’s degree in Economic Development and Growth from Universidad Carlos III de Madrid (Spain) and has an undergraduate degree in Business Economics from Universidad Metropolitana, in Caracas (Venezuela).

Cristóbal Salas

Cristóbal is a Lead Investment Officer, Equity and Mezzanine Finance Investments Team at IDB Invest, which he joined in 2018. He is responsible for developing, negotiating and implementing investment structures that include venture capital. Before joining the IDB Group, he worked as Investment Director at Latin American Partners (LAP). He was on the investment team at LAP México, where he acquired experience in creating, structuring and monitoring investments in various sectors in the region, including transportation, energy, water and sanitation, agriculture and telecommunications. He previously held the position of Vice President at Stephens Cori Capital Advisors. He has extensive experience in investment banking, Latin American markets and management of equity investment funds in the transportation and telecommunications sectors. Cristóbal earned a master’s degree in business administration from George Mason University (USA) and a professional degree in business administration from the Instituto Tecnológico y de Estudios Superiores de Monterrey - ITESM (Mexico).

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeAgribusiness

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.