Sustainability-Linked Bonds Come With Great Perks for Businesses

Sustainability-linked bonds have key perks for issuers including ensuring the walk-the-talk of sustainability and corporate strategies; use of funds for general corporate purposes; investor attraction and diversification; potential ‘greenium’, and others.

Sustainability-linked bonds (SLBs) are the new kid on the block and in a short time have attracted growing interest from the market. These performance-based instrument link the coupon to pre-determined sustainability outcomes that result in material improvements, with no restrictions on the use of proceeds.

This is something we already discussed. But, what exactly are the perks for issuers and how can companies leverage these effectively?

- ‘Walk-the-Talk’ Strategy

By committing to ambitious targets that, if not achieved, result in extra coupon paid to bondholders, companies’ commit to ‘skin-in-the-game’. This is a direct indication to stakeholders on the importance of the corporate sustainability strategy. The clear link between financing and the corporate sustainability commitment empowers this agenda both internally and externally.

Employees with ‘sustainability’ roles that in the past had difficulty approving ESG (environmental, social and governance) initiatives can now leverage the negative consequences of the financing instrument, that is, the coupon penalty. At the same time, individuals in the financial department can get a better understanding of their roles in the company’s ESG agenda.

Externally, companies can express their aspirational vision with credible verification from a Second Party Opinion that benchmarks commitments to best-in-class peers, international standards and references. SLBs give all stakeholders reassurance that key performance indicators (KPIs) are ambitious and credible. This in turn facilitates partnerships.

- Meaningful, tailor-made approach

To-date, the majority of SLBs come out from resource-intensive industries with KPIs relating to environmental and decarbonization targets. But SLBs are not biased towards any specific issuer type.

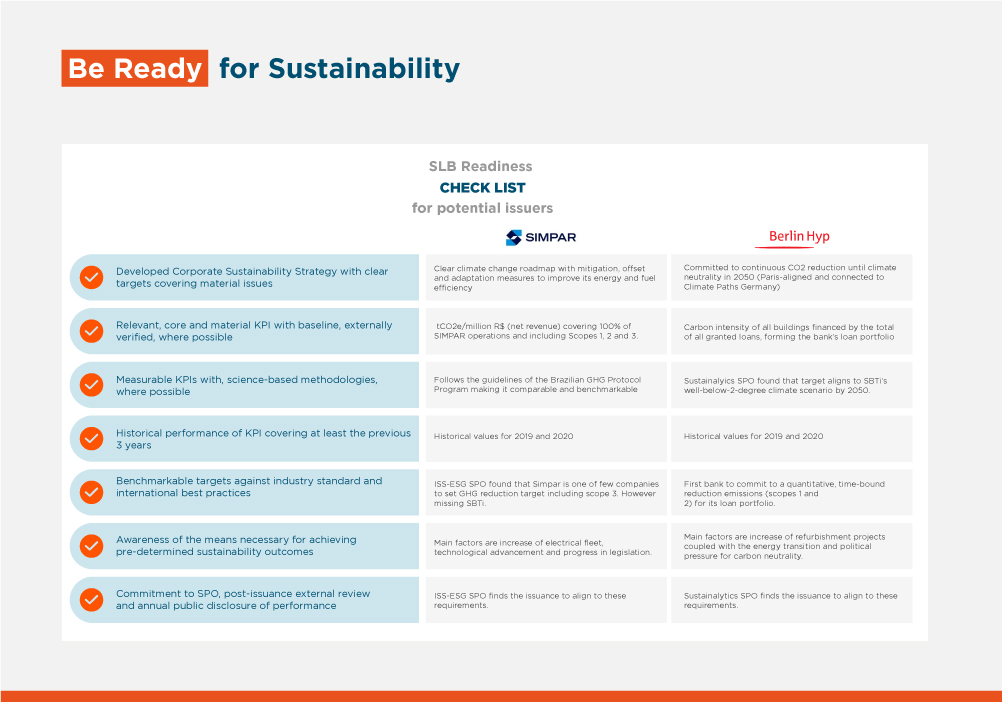

Simpar, a Brazilian transportation company, is committing to reducing GHG emissions; Berlin Hyp is a financial institution pledging a reduction of CO2 emissions on its entire loan portfolio; and Novartis, a multinational pharmaceutical, commits to improving the reach of medicine for patients from low-income housing.

One clear downside is that this flexibility and lack of standardization can result in ‘sustainability-washing’ risks. Thus, companies must choose material KPIs and ambitious targets that shield the issuance from public scrutiny. KPIs must meet the ICMA SLB principles demanding criteria: relevant, core and material to the business; measurable; externally verifiable; and able to be benchmarked against other organizations.

- Use of Proceeds directed at General Corporate Purposes

Before SLBs arrived, green, social, or sustainable bonds were the only thematic instrument available, and they tied proceeds to specific green or social projects. Even though there was interest from companies from multiple sectors, some, due to the nature of their business or insufficient capex pipeline for sustainable projects, would hit a roadblock in their journey towards thematic issuance.

SLBs sever the link between a company wishing to issue sustainable debt and the amount of capex required to meet its sustainability objective. This instrument captures ESG progress holistically, allowing management the discretion to optimize capital expenditure deployment to maximize impact.

This lowers pressure on capex. However, interested businesses should be able to meet minimum requirements by the ICMA’s guiding principles. SLBs should be treated as a complementary financing instrument to traditional thematic products depending on the issuers needs and sustainability journey.

- Diversifying the investor portfolio and inclusion of global ESG investors

Many companies that have come out with SLBs have dabbled in the international debt capital markets before. Regardless of whether you are a first-time or a frequent issuer, SLBs allow for a deeper reach within global ESG investors. This diversification strategy gives companies the opportunity to expand investor relationships and get closer to responsible investors that can ultimately help them stay ahead trends, regulations, and competition, while improving their sustainability strategies.

- Differentiate and Inspire Others

Trailblazing issuers that are leading the way on SLBs are using the instrument to initially differentiate themselves but ultimately are providing tools for peers to follow. This is important since the more issuances established the more interest the investors are showing for these products moving forward.

- Sustainability Kaizen

SLBs force senior management buy-in into setting and reaching sustainable linked KPIs on an on-going manner. This so-called Kaizen (“change for the better”) framework is powerful way to reach meaningful long-term goals by incremental changes.

SLBs should not be a one-off issuance, but an on-going commitment to returning to the capital markets. A clear example is Suzano. The Brazilian pulp and paper company issued its first SLB in 2020 with KPIs associated to a reduction in greenhouse gas emission. The company returned with a second SLB issuance in the second quarter with a coupon linked to industrial water withdrawal intensity and women in leadership positions.

- Cherry on top

SLBs generally benefit from over-subscription and “greenium” – market jargon that unites the terms “premium” and “green”. CapitalReset analyzed this phenomenon in Brazil, the country with the highest number of SLB issuances in Latin America and the Caribbean.

For both pulp and paper issuances, the greenium could be accounted for by comparing the SLB to traditional, vanilla issuances with similar terms and conditions. Suzano’s 10-year $750 million issuance in September 2020 resulted in the lowest interest rate in the company’s history; the gap continued to widen in the secondary market, prompting the company to reopen the issuance two months later. The additional US$ 500 million resulted not only in the lowest interest rate in its history, but also the lowest rate for a Brazilian company for a 10-year international issuance.

Klabin issued in January 2021 a $500 million SLB with a 10-year maturity and 3.2% yield, the lowest for a Brazilian company with BB+ rating. On the same day in the secondary market, the company’s traditional bonds maturing two years earlier were trading at 3.4%.

Even though the market is still under development, SLBs are here to stay. The question business’ should be asking is where should I begin?

Authors

Bianca Conde

Bianca Conde has a double degree in Biology and Marine and Atmospheric Science from the University of Miami and a Masters in Environmental Management from Duke University. She has over eight years of experience in corporate sustainability with a deep knowledge of embedding ESG into corporate strategies and management in systemic and cross-cutting way. Currently, Bianca is the Sustainable Business and MSME Officer at IDB Invest where she supports clients in implementing initiatives that provide for positive impact and contribute to sustainable development in Latin America and the Caribbean.

Carole Sanz-Paris

Carole Sanz-Paris leads the debt capital markets team at IDB Invest. She is a specialist in fixed income, structured finance transaction execution, sale-side research, and credit analysis. She defines herself as passionate about investing with social impact. Carole has more than 20 years of experience in global capital markets; she has been responsible for the structuring, execution and placement of many complex financial structures, including securitizations. She has published extensively on the relative value of fixed income products and credit analysis, having developed her interest in social responsibility and impact investing while earning her Executive MBA from Oxford University.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

Subscribe{{ raw_arguments.field_category_target_id }}

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.