Reaping the Benefits of Subordinated Bonds: The Case of Banco de Bogotá

Subordinated bonds can extend financing to the real sector and priority segments, such as small- and medium-sized enterprises, women entrepreneurs, and green projects that contribute to climate change mitigation and adaptation.

Sophisticated financial instruments can go a long way towards catalyzing the transition to a more sustainable, resilient and fair economy. The first international subordinated bond issue by a Colombian bank, Banco de Bogotá (BdB), is a clear example of that.

These instruments help to extend financing to the real sector and priority segments, such as small- and medium-sized enterprises, women entrepreneurs, and green projects that contribute to climate change mitigation and adaptation.

Founded in 1870, BdB is the oldest financial institution in Colombia and is the main subsidiary of Grupo Aval. It has at least one banking services channel in 957 municipalities, covering 87% of the Colombian territory and facilitating access to products and services in line with its inclusion strategy.

By issuing a $230 million subordinated loan subscribed by IDB Invest, BdB will have additional resources to finance its social portfolio for micro-, small-, and medium-size enterprises (MSMEs), women-owned and -led MSMEs, and low-income priority housing. BdB will also finance green building, renewable energy, energy efficiency, circular economy, and sustainable agriculture projects, among others.

The issuance consists in subscribing sustainable subordinated bonds with a 10-year tenor. The bond proceeds are earmarked to finance specific MSMEs, women-led MSMEs, social housing, and climate projects. Likewise, the bond is considered as Tier II capital or additional equity, thus providing financial soundness to entities by reinforcing their regulatory capital.

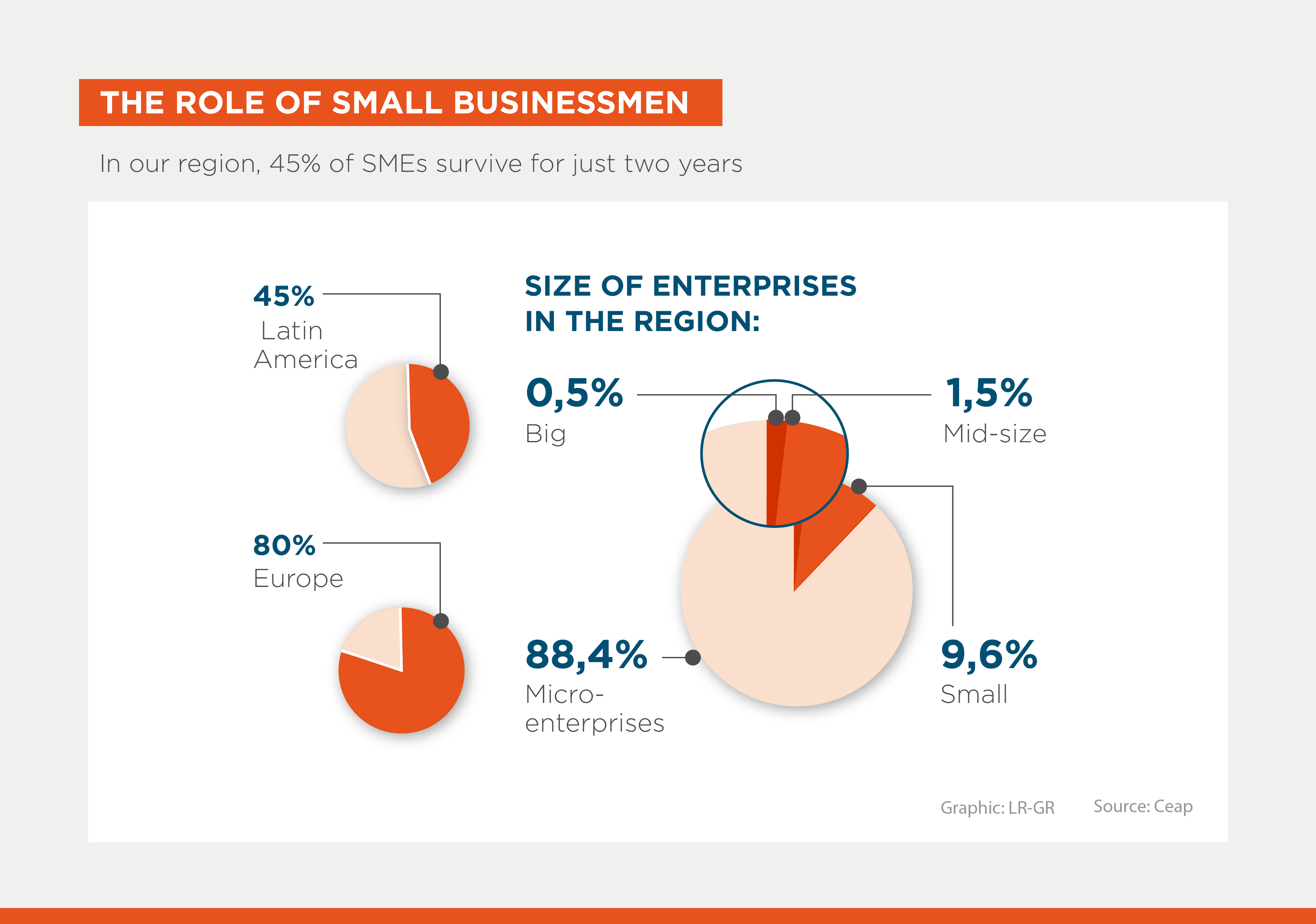

This is key because 95.5% of Colombia’s corporate sector is made up of MSMEs, which account for 30% of GDP and employ more than 65% of the workforce. On the other hand, it is estimated that only 23% of the total housing disbursements are earmarked to finance new or second-hand social housing loans.

The climate approach will include circular economy projects, with an economic development potential amounting to nearly $11.7 billion in annual material savings and the chance to generate new business by strengthening domestic value chains. Current estimates indicate that Colombia will need to invest at least 1.2% of GDP annually in these projects to address the climate challenge.

Structuring the project as a sustainable bond involves defining eligible portfolio categories and developing the so-called Use of Funds Framework. This adds value by setting tangible goals based on project selection, monitoring and assessment criteria that are consistent with the sustainable bond principles of the International Capital Markets Association (ICMA).

All this will help mitigate the impact of loans on women-owned MSMEs located in vulnerable municipalities. Financing resources for these businesses in Colombia are low, particularly when they are owned by women entrepreneurs. In response to this situation, BdB will provide training to commercial advisors on circular economy projects in collaboration with Asobancaria, the Colombian banking and financial entity association.

By designing a model to attract more international capital aligned with the standards and requirements of international entities, additional value is created. In fact, IDB Invest will subscribe $80 million, while the International Finance Corporation will invest $75 million; the Canadian Development Institute, $50 million; and the LAGreen Fund and eco.business Fund, managed by Finance in Motion, $25 million.

Authors

Ana Vera

Ana Rosa Echeverri

Ana Rosa is the Private Sector Coordinator of the Andean Region (CAN). In this position, she has given support to the private sector through the inclusion in the IDB Group's country strategies the implementation activities of the prioritized private sectors. She coordinates the integration of IDB Invest, IDB and IDB Lab teams from various areas, to produce more complete projects, providing more complete financial and knowledge solutions. Ana Rosa supports the development of markets, products, and tools for the private sector of the countries of the Andean region. Ana Rosa was an Investment Officer in Financial Institutions at IDB Invest since 2015. Her main achievements in this position were to originate and structure financial solutions to financial institutions in the region, leading the IDB Group's sustainability agendas on issues such as green, social and gender finance, digitalization and inclusion. During her career at the IDB Group, she has been a Project Portfolio Officer and has been in charge of the credit risk analysis of financial operations in the Transportation, Manufacturing, sectors among others. Prior to joining the IDB Group, she was Vice President of the rating agency Bank Watch Ratings of Colombia and Director of the Financial and Economic Analysis Unit of the Financial Superintendence of Colombia. She also worked with the Foreign Trade Bank of Colombia Bancoldex, in the area of financing regional banks with foreign trade and rediscount lines. Ana Rosa holds a master degree in Finance from Birbeck College, University of London (United Kingdom), as well as a specialization in Investment Project Evaluation from the Universidad de los Andes and an undergraduate degree in Economics from the Universidad Javeriana (Colombia). She is currently pursuing a master degree in Sustainable Development at the Universidad de los Andes.

Sergio Díaz

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeFinancial Institutions

Related Posts

How Santander Brasil and Eco Invest Mobilize Private Capital at Scale

IDB Invest provides financing to Banco Santander Brasil to support sustainable agriculture, land restoration efforts, and resilient infrastructure.

S&P’s AAA Rating Validates IDB Invest’s Strength and Strategic Direction

The AAA rating expands the institution's access to a broader investor base, supporting its ability to finance and mobilize private impact investment in Latin America and the Caribbean.

Beyond the Cash Gap: How Reverse Factoring Is Unlocking Growth for MSMEs

An IDB Invest study in Mexico estimates that adopting reverse factoring is associated with a 27% increase in companies' sales.