Caribbean Financial Institutions Are Looking to Open their Digital Umbrellas

A shift towards greater digitization was overdue for Caribbean banks, and has been accelerated by the current pandemic. Now, they are rolling out their digital channels, seeking to implement ways in which to help bank customers and employees protect themselves while providing the same and enhanced services.

At the best of times, it's no fun standing in line under the Caribbean sun, unless you carry a big umbrella. Now, consider the effect of the new rules of social distancing, making long queues an everyday occurrence outside of bank branches and ATMs, which could be seriously hazardous to your health.

Exactly! A better way to handle banking transactions must be found.

Caribbean banks and multilateral institutions have been thinking long and hard about this, and the emerging solution is something that we might call “digital umbrellas” – ways to help bank customers and employees, and everyone involved in the financial sector, protect themselves from the dangers of the pandemic.

This mostly involves a swift turn towards digitization. Banks now need to provide the same services and more through digital platforms, avoiding direct human contact as much as possible, while still remaining profitable.

The idea makes the best of the current difficult situation. The need for greater digitization in the Caribbean banking sector, and elsewhere, has been evident for some time. Given the pandemic is already causing great havoc in economies and across various sectors as we all balance the choices of lives and livelihood, shouldn’t we all take advantage of the moment to make a digital leap that was overdue, anyway?

You may also like:

-

Sustainability, the vaccine for Latin America and the Caribbean economies

-

Two Successful Models for Promoting Banking Digitalization: The Cases of Colombia and Peru

We're all changing our personal and professional lifestyles to accommodate this disease and any future similar diseases that might come in the future. The banking sector, long an unsung pillar of the Caribbean economies, is also adapting and changing along the way to confront these challenges.

It's a cliché to identify the Caribbean banking sector as offshore institutions and tax havens in some countries, since the reality is that it's so much more than that. Consider the Commonwealth of the Bahamas with its archipelago of seven hundred islands and cays, or the less densely populated areas within the Guyanese interior or Trinidad and Tobago, which is made up of two distinct islands. This presents unique decisions for banks in terms of transportation and logistics, as well as the location of bank branches.

As a people, we all prefer face-to-face services, and the trust and security that comes with interacting with someone on the other side of the counter, but this comes at an increasingly significant cost, which, as customers, we have been unwilling to bear. This, and other reasons, have led banks to consolidate their local presence into regional centers rather than small neighborhood banks.

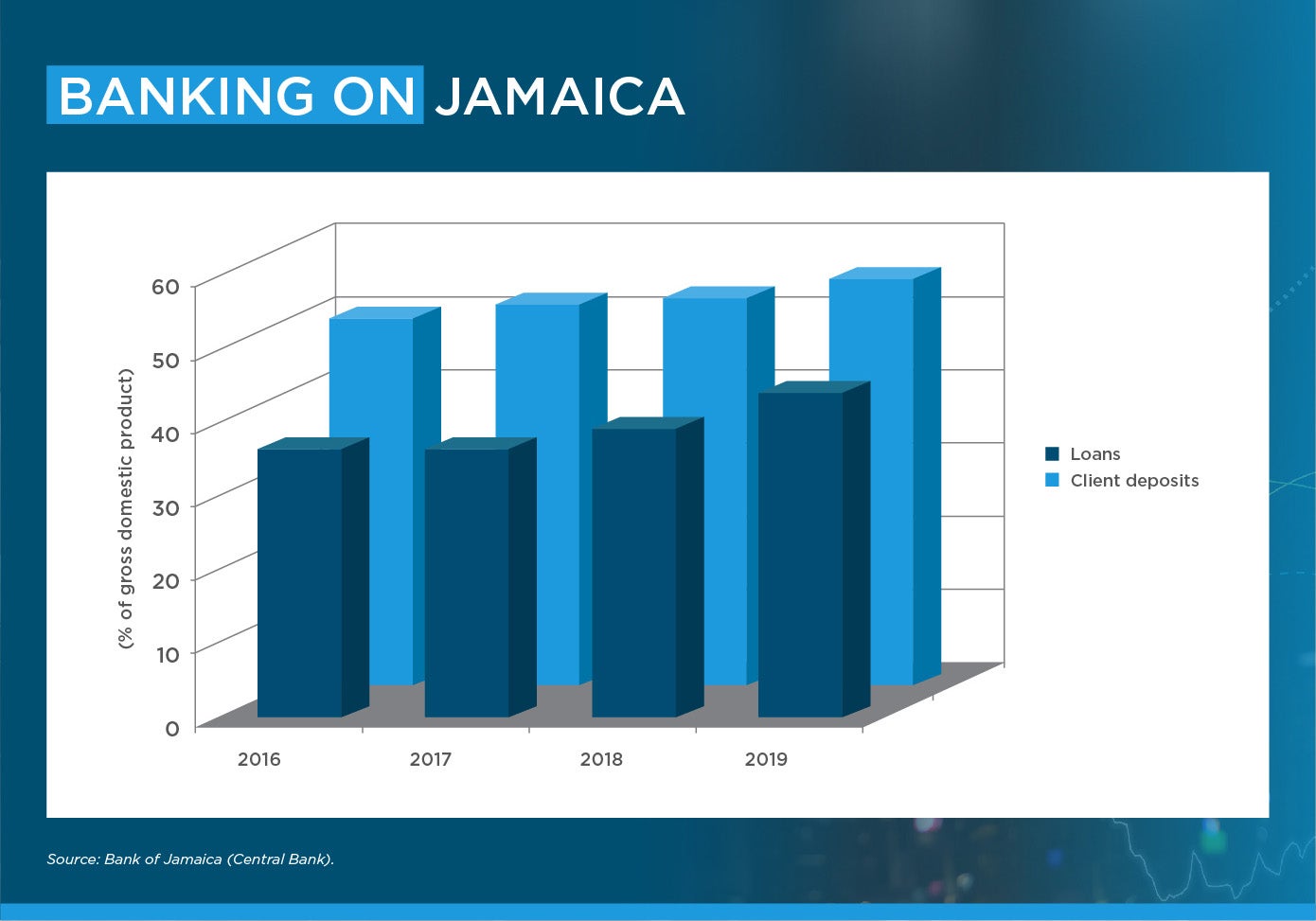

Jamaica is such a case. As the English Caribbean’s second-largest economy, its rugged terrain was historically characterized by some interesting transportation challenges. Despite this deterrent, coupled with the advent of an improved highway network and a more recent sovereign restructuring, the financial sector has been expanding steadily, providing much-needed credit and attracting increasing deposits in the past few years, and has plenty of room to future growth.

On a wider scale, the Caribbean financial sector was already facing significant challenges when the pandemic hit. Canadian banks such as Bank of Nova Scotia, Canadian Bank of Commerce and Royal Bank of Canada, huge players in recent years, have been reducing their regional footprints by selling off their operations, which has presented growth opportunities for some regional indigenous banks, but the fundamental issue still remains. How best to scale banking operations in home and remote markets, now in an ever-changing global landscape, to provide cost effective banking products and services to customers?

The road towards digitization, though unclear, is not out of the reach of many of the region’s financial institutions. While much of the developed world has made huge investments in this area, not all of them are still relevant today. This presents a wonderful opportunity for the region to learn quickly from the past experiences of others, and quantum leap in order to catch up. And there is help for banks embarking upon this journey. IDB Invest, the private sector arm of the IDB Group, can lend assistance here. Partnering throughout the Caribbean and Latin America for the past sixty years allows this developmental organization to share varied experiences and tailor solutions to banks and other organizations where, as we know in Caribbean region, one size doesn't fit all.

A good example of this is the recent seven-year subordinated loan agreement for $75 million with Republic Bank in Trinidad & Tobago. IDB Invest funds are being directed to support the lender's digitization, as well as execution of its plans for increasing the size of its retail portfolio by providing small and medium-sized enterprise loans and housing loans for middle-income families. The partnership is expected to help Republic Bank’s consolidation as a leading financial institution across the Caribbean region, as part of its expansion strategy.

Such steps, and others yet to be taken, are bound to help a region that can really use a good digital umbrella right now. It's time to walk the walk, even if it's a digital one.

Authors

Stephen Thomas

Stephen leads the Financial Institutions Team for the Caribbean region at IDB Invest, which he joined in 2019. He is responsible for originating and structuring financing transactions for financial intermediaries that have an impact on development, by increasing access to financing, fostering women’s empowerment and supporting climate change mitigation programs, among others. Before joining the IDB Group, Stephen led teams focused on equity brokerage, investment advisory and wealth management for First Citizens in Trinidad and Tobago, St. Lucia and Barbados. He previously worked as Debt Capital Markets Head of Citicorp Merchant Bank Limited, covering clients across the wider English-speaking Caribbean region. Stephen earned a master’s degree in business administration (MBA) from the McDonough School of Business at Georgetown University, Washington D.C. (USA) and an undergraduate degree in economics from the University of the West Indies.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeAgribusiness

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.