Can Korea's Digital Transformation Be Applied to Latin America and the Caribbean?

Korea's digital transformation has been effective in responding to the pandemic and helping sustain economic and social development. Korea’s experiences regarding digital transformation provide insights for Latin America and the Caribbean.

South Korea has been one of the most successful countries in responding to the COVID-19 crisis. Korea has prevented the pandemic while turning the economic crisis into an opportunity for growth, as a result of long-term investment in Information communication and technologies and an ecosystem of digital transformation.

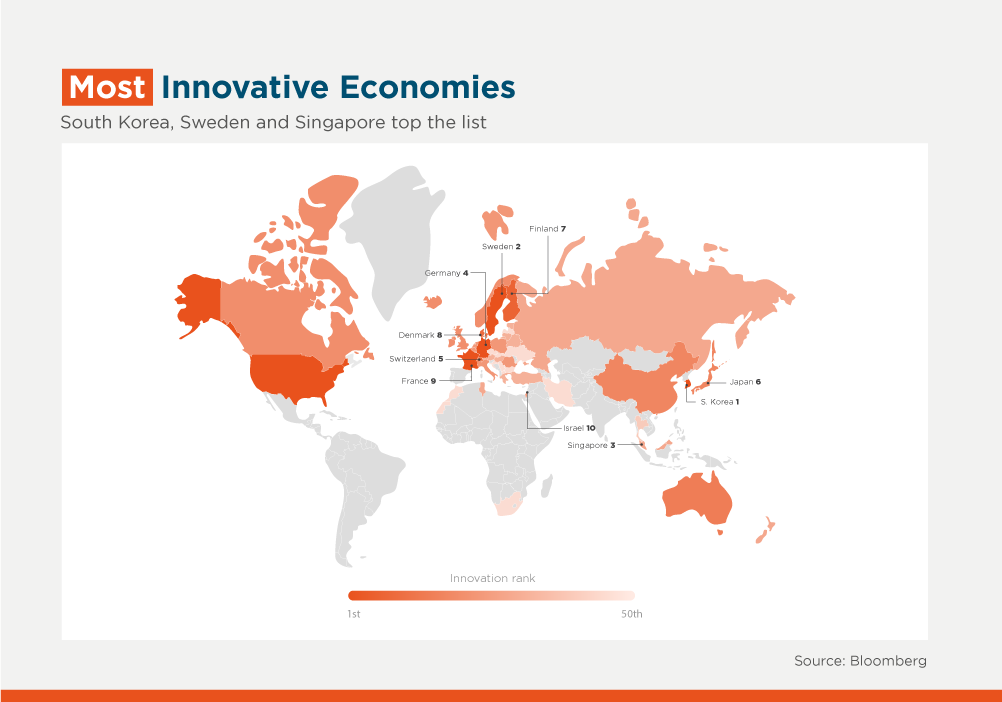

At the same time, Korea's digital transformation is highly regarded in the international community. The Bloomberg Innovation Index released in February 2021 ranked the country first among 60 surveyed.

The question, then, is whether Korea's digital transformation experiences be applied to Latin America and the Caribbean (LAC). And the answer is that there are five insights from Korean examples that can be valuable for LAC’s digital transformation:

1. Leadership at the top level is essential for digital transformation. This is because the company's executives know the need for digital transformation and require active mid-to-long-term investment decisions to drive it. For example, in Korea, a digital transformation began with large corporations such as POSCO and LG, driven by bold decisions by top executives. Based on this investment in innovation, today's large Korean companies are playing key roles in the global supply value chain that drives and sustains the global economy.

2. Digital transformation can contribute to the development of innovative business models for SMEs to enhance their competitiveness. For example, Market Kurly in Korea is an example of ordinary food distributor that has transformed itself into an online-based fresh food delivery company. Using big data analysis based on customers’ data, they created a new business model under which, if customers order by 11 pm, the company delivers the fresh food by 7 am the next morning. This disruptive business model has been extremely successful, and even large retailers in the Korean market are benchmarking this innovative approach.

3. Digital transformation is possible by individuals with a motive to innovate. For example, an online class platform company called Classting in Korea was created by an elementary school teacher who was dissatisfied with offline class management. In Classting, teachers can conveniently share announcements, class materials, photos, and videos, easily develop learning materials, and manage assignments submitted by students. Also, they came up with 'Classting AI', an artificial intelligence (AI) tutor that helps pupils study at school more easily. This AI-powered platform is currently in service in 15 countries.

4. Digital transformation can provide an innovative way for solving problems in sectors that are not always seen as technology-based industries. For example, the agricultural sector, threaten by the climate crisis, can be helped with digital transformation. A Korean company called N.THING is a smart farming concern that developed a 'Planty Cube' that can grow vegetables such as romaine and lettuce and herbs in a smart container, as if in a greenhouse. It’s based on the Internet of Things (IoT) and AI, and can save more than 98% of water compared to conventional farming. In addition, the containers can be stacked up to three stories high, so they don’t require a large area of land, and there is little of the ecological impact brought about by traditional farming.

5. Digital transformation increases the need for international business development, international cooperation, and global partnership. In this context, digital transformation is an important topic for cooperation between Korea and LAC. Korea and LAC have already collaborated on digitalization through various channels including the Korea-LAC Business Summit, Korea-LAC Startup Pitch Day, and LAC-Korea Deep Tech Exchange Program. The more the merrier.

In addition to the five insights presented above, if you want to know more about Korea’s digital transformation experiences, you can check this publication: Research on the Digital Transformation and Ecosystem of Korea applicable to LAC companies.

Authors

Sung Nam Choi

Sung Nam Choi is a professional in IT projects for development. Before joining IDB Invest, he worked as a principal manager in the National Information Society Agency (NIA) of the Republic of Korea. He led IT projects for developing countries such as national digital agenda, broadband masterplan, e-government systems & applications, and digital inclusion policy. In addition, he conducted IT advisory services and managed IT training programs collaborating with international organizations like International Telecommunication Union (ITU), Asia-Pacific Telecommunity (APT), Asian Development Bank (ADB), African Development Bank (AfDB), and Inter-American Development Bank (IDB). Furthermore, he has 7 years of field experience in Nicaragua and Costa Rica. He launched the first virtual Spanish IT education platform (CEABAD, https://ceabad.com/, located in Nicaragua) for policymakers, experts, and college students in Latin America. He coordinated over 30 MOOC (Massive Open Online Course) including digital business, e-commerce, Fintech, Internet of Things, Cloud Computing, Artificial Intelligence, and Blockchain technology through this platform. He also served as the representative of the Office of KOICA (Korea International Cooperation Agency) in Costa Rica. He studied a Ph.D. in Public Administration at Korea University, earned a master’s degree in Public Administration from Yonsei University (Korea), and completed the Executive Education Program of Digital Transformation in Government at Harvard Kennedy School (USA).

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

Subscribe{{ raw_arguments.field_category_target_id }}

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.