As ESG Investors Look for Returns, Sustainability-Linked Bonds are the Hot New Thing

SLBs are new type of ESG-friendly bonds with variable coupons tied to sustainability targets. As opposed to green, social or sustainable bonds, issuance proceeds are not tied to specific green or social projects or assets; the focus is on the company’s ability to meet its commitments.

OCTOBER 29 2021

Investors concerned about environmental, social and governance issues (ESG) are looking for new types of investment instruments. Enter sustainability-linked bonds.

These bonds – commonly referred to as Sustainability-Linked Bonds, or SLBs – provide an interesting new wrinkle for ESG investors looking for returns. As opposed to green, social, or sustainable bonds, SLB issuance proceeds are not tied to specific green or social projects or assets; instead, issuers of SLB pledge to improve their performance against specific sustainability targets and indicators and link their sustainability commitment to the coupon paid to bondholders.

SLBs involve setting sustainability Key Performance Indicators, or KPIs, and targets for the issuer, which are linked to a reward if targets are met (step-down in coupon payment) or penalties if they are not (step-up in coupon payment, so more return for the investors and a higher cost for the issuer). KPIs, therefore need to be credible, meaningful, impactful, objectively measurable and verifiable, as well as comparable against industry benchmarks. Overall, KPIs are critical in determining SLBs that truly foster sustainability, raise ambition and go beyond business as usual.

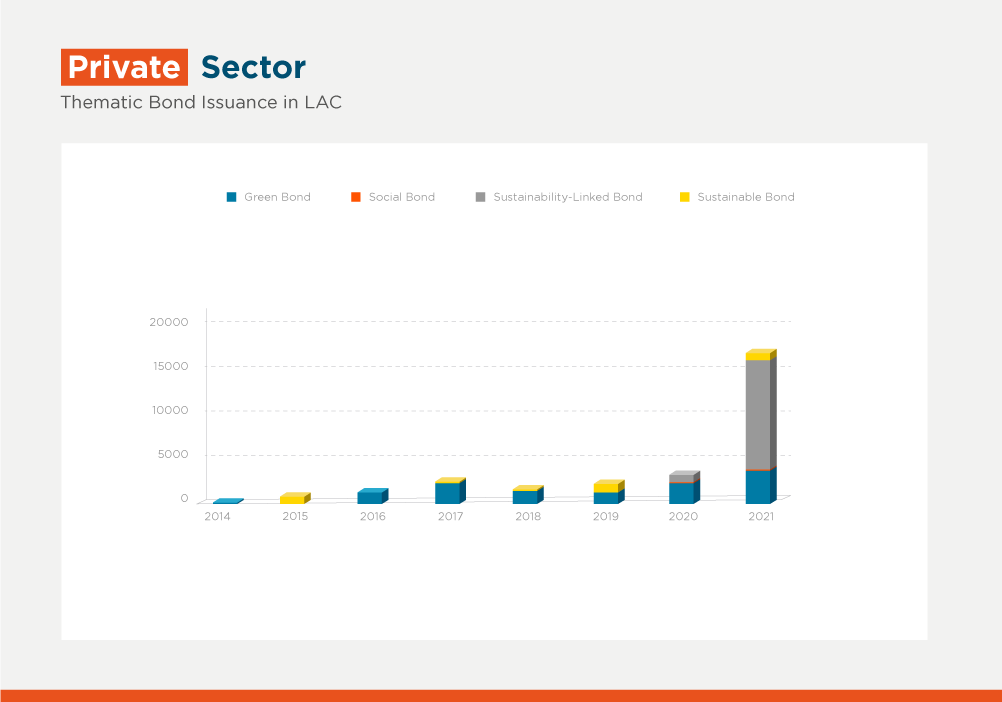

Since the world-first SLB in 2019, this new asset class experiences increasing global relevance compared to traditional “use of proceeds” thematic bond. SLBs represent about 15% of global thematic bond issuance year-to-date. In Latin America and the Caribbean (LAC), SLBs are gaining predominance, representing about a third of overall thematic bond issuance and three quarters of thematic debt issuance by the private sector. In the first 9 months of 2021, $12 billion out of $16 billion worth of thematic bonds issued by Latin American corporates were SLBs.

This SLB dominance stems from a convergence of interests: growing global investor demand for ESG investment; increased scrutiny in linking risk and performance, as well as in driving strategic sustainability as opposed to one-off projects; and, from the corporate side, less capex pressure – they are an opportunity to attract new capital linked to key performance indicators and targets that are in line with their material ESG issues and their overall sustainability strategy.

SLBs in the region tend to be concentrated towards large corporates already advanced in their sustainability strategy, such as Klabin, Suzano or Simpar. These successful SLB issuers all benefit from long historical performance, sustainability goals and internal protocols to measure and self-report their sustainability performance. Coincidently, these corporates were already known to the international debt capital markets, and SLBs allow for a deeper reach within global ESG investors. By contrast, local ESG investors base is growing in our region but remains limited.

There is an undeniable opportunity for companies not-yet known in the global debt capital market to integrate long-term sustainability into their operations and appeal to ESG investors. There is a role for a multi-lateral development bank like IDB Invest to support clients in strengthening and further integrating sustainability in their business strategy, defining, measuring and disclosing material and ambitious KPIs; culminating in an eventual SLB issuance.

IDB Invest also supports the local SBL market development by educating investors on how integrate ESG into their investment criteria and providing the appropriate valuation tools and frameworks. At IDB Invest, we view the issuance of SBL in local markets as a critical stepping stone for many companies, towards successful international issuance.

SLBs are gaining much traction, and the market has benefitted from ICMA’s guiding principles. But there remains continuous need for improved standards to appeal to more ESG investors (both globally and locally). Such standards do not have to compromise on the product flexibility offered to issuers who are able to integrate sustainability strategies into their broader operation.

Considering that there are no standardized sustainability targets or indicators for SLBs, the majority of KPIs for SLBs issued in LAC have been related to environmental and decarbonization initiatives from companies in transportation or pulp. However, SLBs lend themselves well to incorporate other relevant social, sustainable KPIs. A recent example was the issuance by Brazil’s exchange operator B3 which incorporates KPIs for women in leadership of listed companies and development of a diversity index.

The flexibility offered by SLBs comes at a price of designing measurable and achievable KPIs – the sustainability targets. The trade-off between better funding costs achieved and additional cost of devising and implement the sustainability KPIs is only positive where economies of scale can be achieved.

For smaller SLB issuers, this balance can be uneconomical, especially in international debt capital markets. The KPIs need to reflect the right price incentive to induce a positive behavior change. Ambitious targets of SLBs are key to ensure successful outcomes. But ambition must be priced accordingly for the issuers to be willing to go the extra mile. The benefit must compensate for some of the costs associated with changing the issuer’s behavior (for example, investment in new technology). IDB Invest guides issuers in crafting their company specific Sustainability Performance Targets with the flexibility to tailor their pricing incentives.

Latin America is appealing to ESG bond investors as the region’s potential for impact is greater than in developed markets. Given how large ESG investment allocations are, and LAC potential to establish itself as a key investment destination, it is the perfect time to local companies to consider their sustainability-linked opportunities.

Authors

Carole Sanz-Paris

Carole Sanz-Paris leads the debt capital markets team at IDB Invest. She is a specialist in fixed income, structured finance transaction execution,

Paula Peláez

Paula Peláez is the head of SMEs (small and medium-sized enterprises) and sustainable businesses at IDB Invest. She has been head of Business Call

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeGender

Related Posts

A Few Very Good Reasons to Protect the Integrity of Gender Bonds

Latin America and the Caribbean has become a leading region in gender bond issuance aimed at bolstering women’s empowerment. These instruments offer a promising capital market solution to mobilize funds towards projects that help accelerate parity.

How Can We Advance Gender Equality in the Private Sector? Financial Incentives May Help

There is no shortage of women with the leadership qualities needed to run a business or excel in the workplace. What’s often missing are the opportunities to do so. Performance-based financial incentives can help fill this gap by motivating companies to advance gender equality in their operations.

Women, Risks, and Opportunities

Women have demonstrated ample evidence of strong leadership. Furthermore, from positions of leadership, we have successfully taken and successfully managed risks time and again. As entrepreneurs, we save more and pay better as an asset class. However, there is still much to do to achieve gender parity.