Revolution 4.0: What's Our Region's Financial Sector Role in It?

The transformations of the Fourth Industrial Revolution now require rethinking the responses to the demands of an economy that is changing by leaps and bounds. Latin America and the Caribbean expect much from the financial sector, but what exactly?

The reality of the Fourth Industrial Revolution (also called Revolution 4.0) affects all areas of our lives all over the world: how we produce and trade; how we move about; how we seek financing; etc. Technological advances are a substantial part of this new paradigm, promising exponential impacts in terms of productivity and growth. Without the active and efficient intervention of the banking system, this process of reconversion could be delayed, particularly in the case of SMEs.

Let’s see a concrete example. According to recent research conducted by CIPPEC, INTAL-IDB and UIA in Argentina, the structure of the manufacturing industry is shaped like a mountain, a mountain being scaled by three groups:

- Trekkers: these represent nearly half the firms that make up the group characterized by having outmoded technology, that are not taking action to reverse this lag, and are mostly SMEs.

- Condors: these companies are on the opposite end from the Trekkers and represent a small segment –6 percent– made up of firms with advanced technologies that are generally taking actions to approach the 4.0 frontier.

- Mountaineers: this is a group of companies –45 percent– with intermediate technologies that appear to be dynamic in reducing their technological lags

The good news is that four out of every ten companies is evaluating or developing actions plans in this regard, meaning that they are aware that advancing toward industry 4.0 is not an option but rather a need as well as an opportunity.

A similar study done by CNI in Brazil shows that the percentage of companies that are taking corrective actions to adapt technologically is three times higher than in Argentina. Another study, supported by the IDB in Uruguay, concludes that most companies are prone to innovate in this country, 68 percent implemented a new process in their business or improved an already existing process in the last year.

Industry 4.0 is a banking business opportunity

When analyzing the main obstacles faced by companies in Argentina, Brazil, or Uruguay and researching the factors affecting their performance and adverse climates for reaching the technological summit, the first factor that emerges –as was to be assumed and without distinction– is the lack of access to financing. Other barriers that emerge with high frequency are the lack of trained human resources and inadequate digital infrastructure.

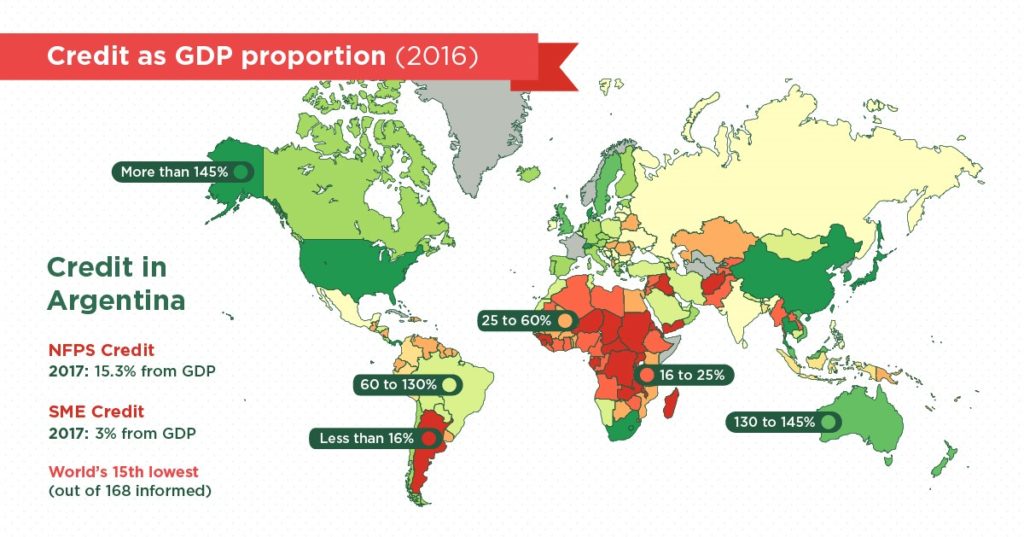

With different nuances, the transition to industry 4.0 has already begun all over the world. But there is an obvious missing link, an essential link in the chain that relates to development of the financial system and access to financing. Argentina is among the countries with the least financing for the productive sector globally; credit to the private sector represents 16 percent of gross domestic product (with the peculiarity that SME credit is equal to only 3 percent of GDP). This percentage is 27 percent in Uruguay and 62 percent in Brazil. Without an adequate supply of funds (volume, term, and specific instruments), companies will not be able to achieve this technological reconversion.

The financial system should view Revolution 4.0 as a business opportunity in which it can support companies, whether SMEs or large enterprises, in their climb toward the technological summit.

This technological revolution occurs more easily in corporate companies, but it becomes more difficult in medium and small companies. Banks can play a fundamental role as “brokers” of information and technology for these SMEs, being able to support the design of reconversion plans that can then be financed by the same bank with appropriate rates and terms. In Europe, BBVA recently launched the digital loan (D-Loan) that seeks precisely to encourage companies to accelerate their digital conversion with an innovative financial product whose price depends on the borrower's digital maturity level.

It is here that multilateral banks, such as IDB Invest, can assist banks in a technical and financial way to support the design of innovative products to meet the demand of this unattended market. The technological reconversion will allow companies to endure over time and grow in a healthy way being more efficient and profitable, which will open the doors to a business model where both actors win, both the firms and their related banks.

The banking system has the opportunity to respond to this missing link and lead this paradigm change in the industry by becoming strategic partners for their clients and not just financiers, which will result in an economy that is more integrated in the world as well as larger, more modern, and more productive.■

Authors

Diego Flaiban

Diego leads the Financial Institutions Team for the Southern Cone at IDB Invest, which he joined in 2016. He is responsible for originating and structuring financing operations for financial intermediaries that have an impact on development. Diego has more than 15 years of experience in the IDB Group, where he has led transactions for loans, capital markets and capital investments in the region that promote access to finance, women’s empowerment and climate change mitigation. Before joining the IDB Group, he worked as Senior Consultant and Auditor of Financial Institutions at Arthur Andersen and Deloitte. He previously worked as a loan officer and financial specialist at leading financial institutions in Argentina. Diego earned a graduate certificate in international business from Georgetown University (USA) and an undergraduate degree in public accounting from Universidad de Buenos Aires (Argentina).

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

Subscribe{{ raw_arguments.field_category_target_id }}

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.